The Misuse of Data Behind the 'Greedflation' Narrative

There's no evidence that greed is causing inflation.

HD DownloadEarlier this year, dictionary.com added the word "greedflation" to its list of actual words, which it defines as, "a rise in prices, rents, or the like, that is not due to market pressure or any other factor organic to the economy, but is caused by corporate executives or boards of directors, property owners, etc., solely to increase profits that are already healthy or excessive."

A nonprofit called Groundwork Collaborative, with the mission of driving "policy change with credibility, expertise, and impact," claimed credit for helping push "greedflation" into the common political parlance. They might be right. The group authored a widely cited study that purports to show how outsized corporate profits have caused rising prices. And the paper is just as economically illiterate as the concept of "greedflation" at its core. The authors misrepresented and cherry-picked data, and they misunderstood the meaning of a key economic indicator.

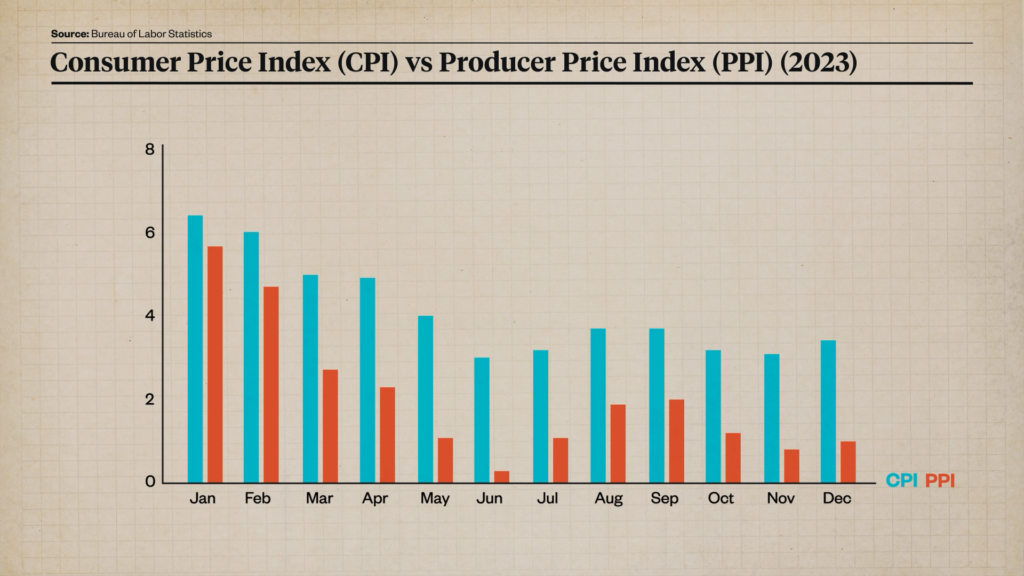

This study, which the Cato Institute's Ryan Bourne has also written about critically, was co-authored by Liz Pancotti and Groundwork Collaborative's Executive Director Lindsay Owens. They found that "prices for consumers have risen by 3.4 percent over the past year" while "input costs for producers have risen by just 1 percent." This is supposedly evidence that corporations are "exploiting their pricing power" to drive up the cost of goods and services.

With this chart, Owens and Pancotti presented further evidence that companies are spending less and earning more. It shows that in 2023, the Consumer Price Index consistently grew faster than the Producer Price Index. Owens and Pancotti interpret this to mean that for U.S. corporations, the prices they charged outpaced their input costs.

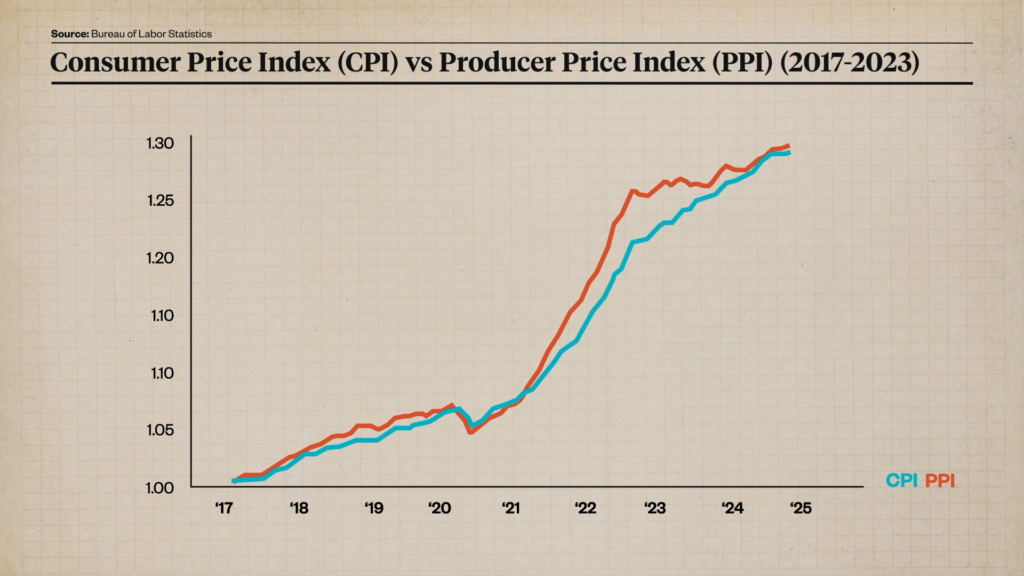

The first problem is that Owens and Pancotti cherry-picked a one-year timeframe to tell a misleading story. Here's that same data in the form of a line graph.

In the period that they chose to highlight, the Consumer Price Index was growing faster. But if you pull back, you see that the prior year the Producer Price Index grew faster. In 2023, the Consumer Price Index was playing catch up. Now the two are roughly in sync.

Owens and Pancotti misrepresented the data by cherry-picking one year, but it doesn't matter either way for the point that they were trying to make. That's because they also misunderstood the meaning of the Producer Price Index. It measures the prices at which producers sell their products to wholesalers; it doesn't measure input costs, or what companies spend making their products. It's a price index, not a cost index. So comparing it to the Consumer Price Index tells us nothing about corporate profit or "greedflation."

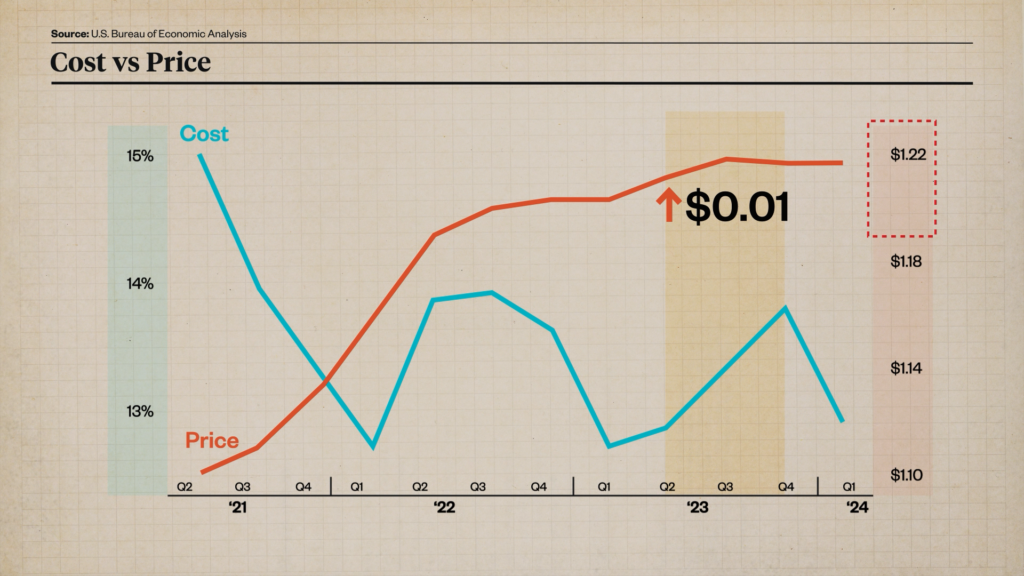

Owens and Pancotti included additional evidence to support their claim. They claimed "that corporate profits drove 53 percent of inflation during the second and third quarters of 2023." By analogy, that means that if the price of a can of chili went up by a dollar, the company spent 47 cents of that extra income paying workers, raising cows, tomatoes, beans, and so on, leaving a whopping 53 cents in pure profit—an example of "greedflation."

Again, Owens and Pancotti cherry-picked a specific time period to get a headline-grabbing result.

This chart shows the corporate profit margin in blue—what for a can of chili would be the selling price to the consumer minus the cost of the cows, the beans, the tomatoes, etc., plus wages paid to workers—versus the price that companies are charging in orange. We can see that in the period the authors have highlighted (shown in light colors) prices barely budged.

Corporate profits may have risen, but it's a large share of a tiny amount. By analogy, even though corporate profits accounted for 53 percent of the increased cost of a can of chili, the price only went up by something like a penny. That means corporate profits drove up the price of chili by about half a cent. It didn't have much impact on American wallets.

If you take a longer view, you see time periods in which prices were rising while profits were falling, like the second quarter of 2021 to the first quarter of 2022, and the third quarter of 2022 to the first quarter of 2023, which the study authors didn't mention. The biggest price climb happened prior to the second quarter of 2022 when profits were going up and down. Owens and Pancotti focused on the second and third quarters of 2023 because they knew it would yield a headline-grabbing number.

But were workers getting cheated?

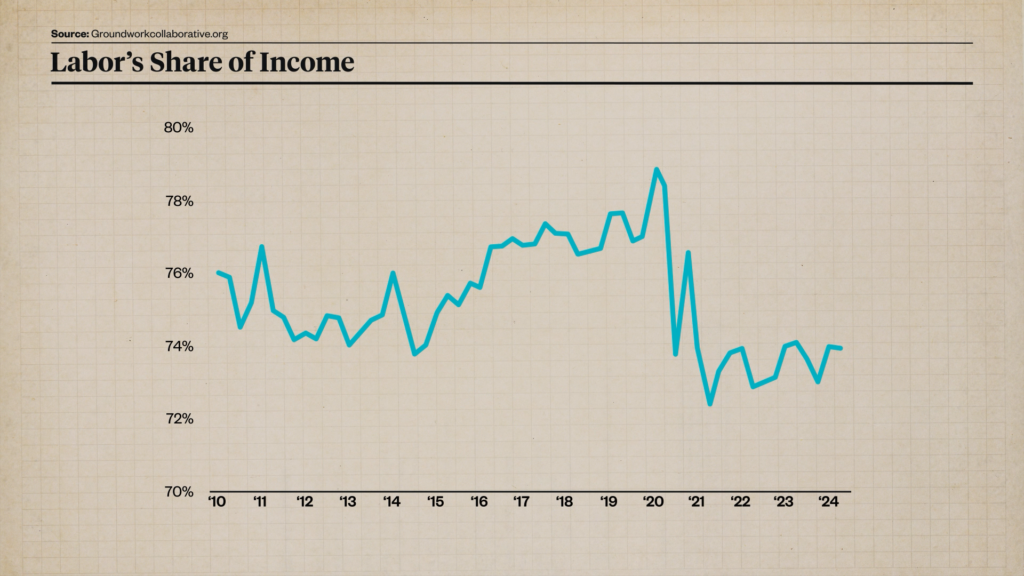

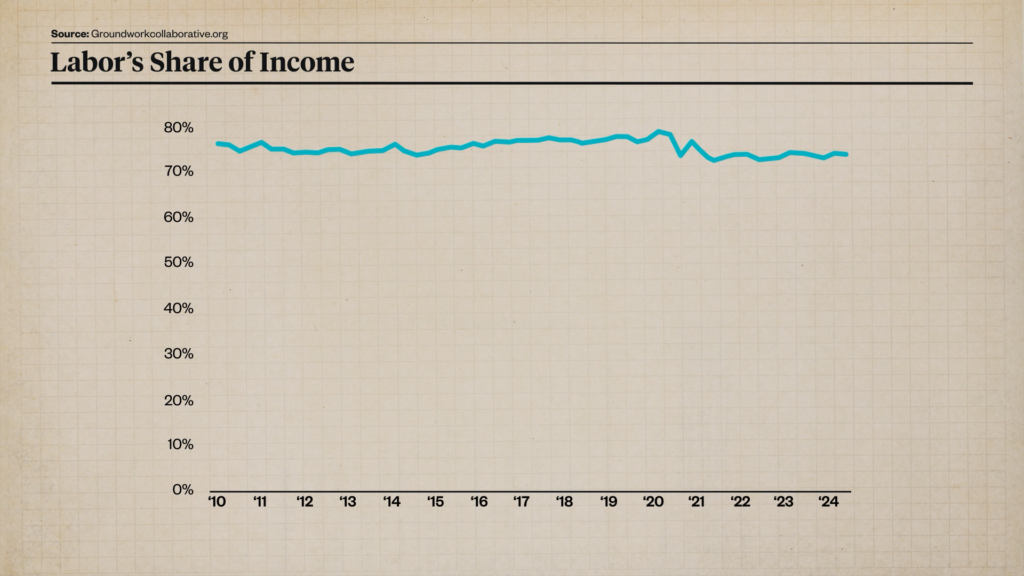

The study also claims that less and less of what companies earn is going to workers' compensation, as illustrated by this chart, showing a declining labor share of income starting around 2020.

Again, this is a cherry-picked time period. Here is the same data going back to the 2008 financial crisis.

Owens and Pancotti also use a common trick to exaggerate changes. Their graph uses 70 percent as the zero point on the Y-axis. Here is the same graph with the correct zero point.

But there's still a decline…so what happened? COVID-19! Lockdowns and economic turbulence brought a significant drop in what workers were earning. But since the second quarter of 2020, long before inflation became a major problem, labor's share of earnings has held fairly steady. And it's hovering around the average of what it's been since the 2008 financial crisis.

Sen. Bob Casey (D–Pa.), who's an ally of Vice President Kamala Harris, has been particularly outspoken about greedflation.

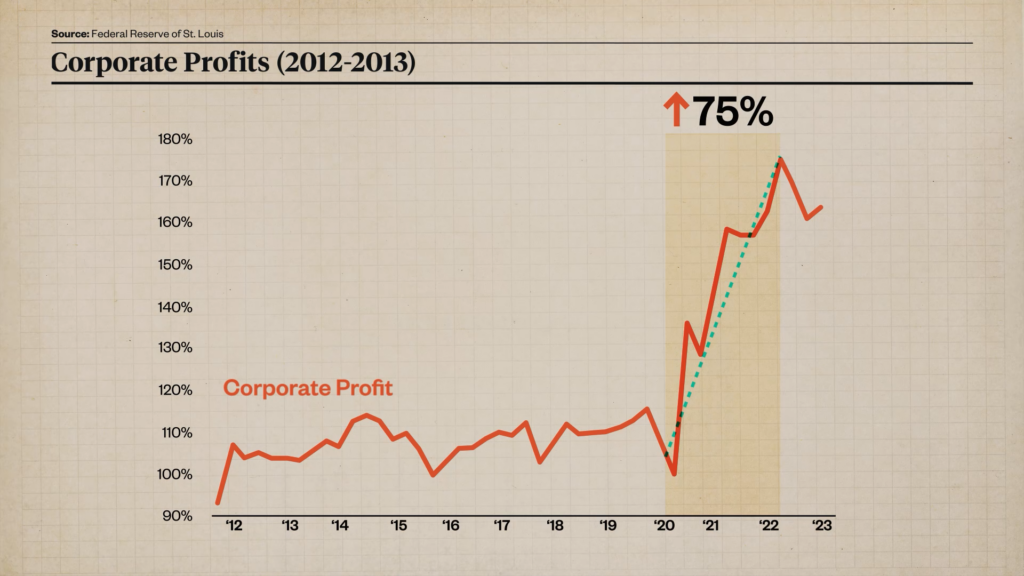

Casey published his own flawed economic research on the topic, claiming in one report that "[f]rom July 2020 through July 2022, inflation rose by 14 percent, but corporate profits rose by 75 percent, five times as fast as inflation."

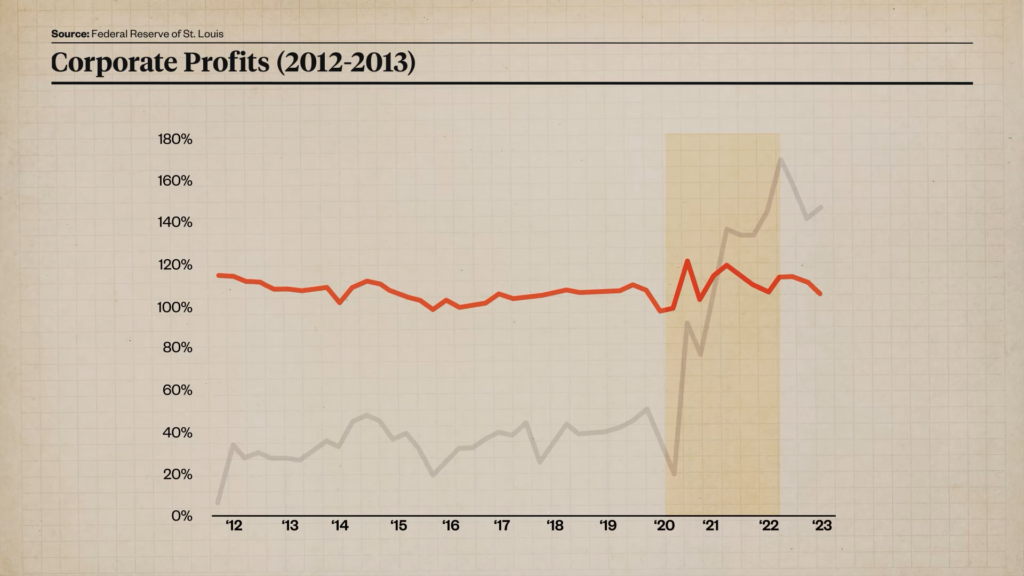

He sourced that claim to this chart from the Federal Reserve of St. Louis, which looks dramatic.

Casey uses the same non-zero Y-Axis scale as the Groundwork Collaborative graph.

Here's how it should look.

OK, but it still looks like corporate profits shot up after 2020.

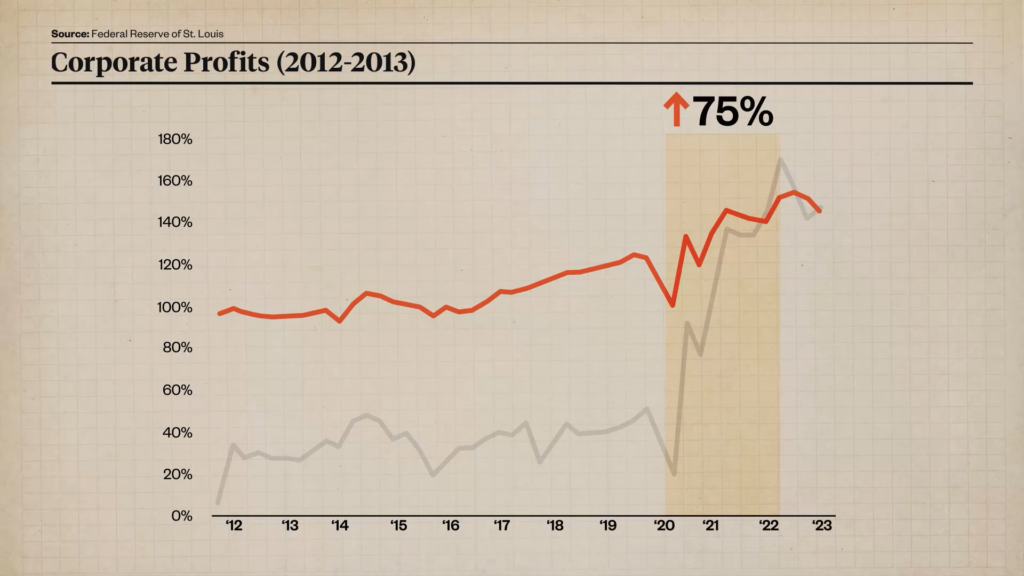

The problem is that Casey chose to use a different measure of corporate profit than the U.S. Bureau of Economic Analysis (BEA). Unlike the BEA, he didn't adjust his top-line figures for what's known as inventory valuation and capital consumption adjustments, which distort the data if you don't correct for them.

Consider a company that makes its product for $0.93 and sells it for $1.00, about the average profit margin for U.S. businesses. Now, 14 percent inflation comes along and the selling price goes up to $1.14. Since the $0.93 costs have already been incurred, the paper profit goes up to $0.21, or from 7 percent to 18.4 percent. But the purchasing power of the $1.14 the company gets is the same as the $1.00 it would have received had there been no inflation. Its real profits have not increased but its corporate taxes probably will.

If we look at things in economic terms rather than simple accounting, we have to acknowledge that the value of the inventory went up 14 percent from $0.93 to $1.06. The company spent $0.93 making it, but that was $0.93 in dollars with 14 percent more purchasing power than current dollars. Moreover, its capital investments in factories, trucks, farmland, or other assets were also made in old, uninflated dollars, so the depreciation expense for those assets should be increased by 14 percent for consistency. This is why inventory valuation and capital consumption adjustments are particularly important in times of high inflation.

If we take those adjustments into account and use the BEA's official numbers, here's how Casey's chart looks:

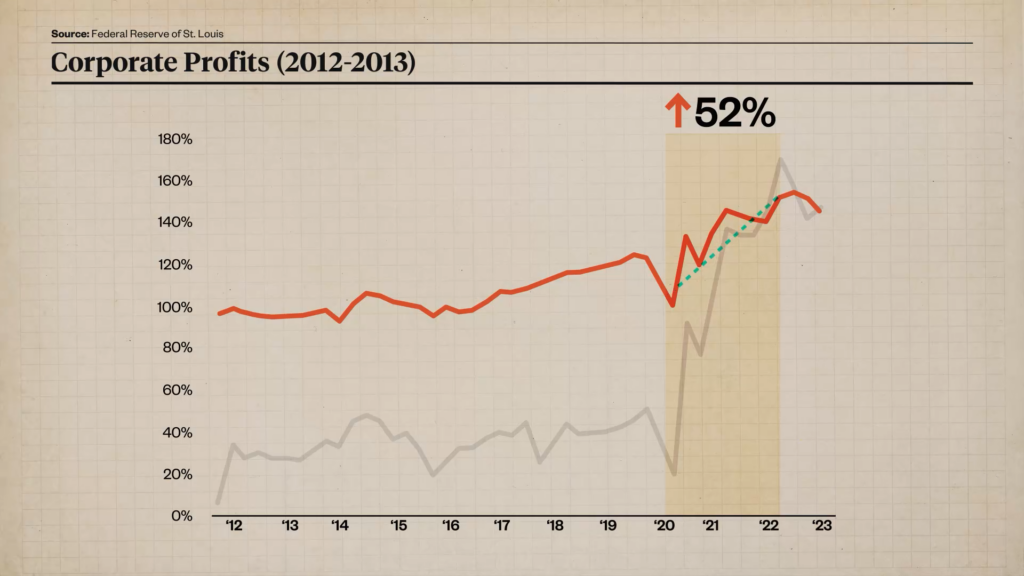

Corporate profits didn't rise by 75 percent during this two-year period, as Casey claimed—but they did rise by 52 percent, which still sounds like a lot.

But now we can also see a different story in the data: Corporate profits have been rising since 2016, with a brief interruption and some volatility during the pandemic. They've been growing because the U.S. economy has been growing—corporations sold more goods and services, workers earned more money, and the economy was running faster.

That's why it makes sense to look at corporate profits as a fraction of domestic income. If we make that adjustment, the graph looks like this:

Now most of the effect that Casey trumpeted has disappeared.

Politicians and activists claim that corporate profits are causing inflation, but the real story is that inflation is creating mostly fictitious accounting profits and tax headaches for corporations. Overall, corporate profits remain pretty stable as a share of domestic income.

During his speech at the Democratic National Convent, Casey said, "We're fighting for honesty…will you fight for it?" Casey should take a look at his own data as part of that fight. Greedflation may be an effective political talking point, but there's nothing honest about it.

Photo Credits: Tom Williams/CQ Roll Call/Newscom, Midjourney

Music Credits: "Liminal Space," by Theatre of Delays via Artlist; "Blue Beings," by Tamuz Dekel via Artlist; "Fragments," by Tamuz Dekel via Artlist.

- Graphics Producer: Adani Samat

- Assistant Editor: César Báez

- Audio mixing: Ian Keyser

- Camera: Cody Huff

- Camera: Justin Zuckerman

- Graphic Design: Nathalie Walker

- Color Correction: Cody Huff