Washington's Debt Delusion: Economic Growth Cannot Fix the Deficit

Republicans are betting trillions on the hope that the economy will grow fast enough to cover their deficit spree.

Washington is running its largest peacetime budget deficit in American history. The national debt held by the public has leaped from 40 percent of the economy in 2008 to 100 percent today—on its way towards 250 percent of gross domestic product (GDP) within three decades. At that point, interest alone would consume two-thirds or more of all federal taxes. And yet, even as a nervous bond market is pushing up interest rates, President Donald Trump—who enacted $8 trillion in spending hikes and tax cuts in his first term—proposes doubling down with even more tax cuts and spending expansions.

How can Washington possibly pay for trillions more in promises on top of this unsustainable debt? According to Republicans in Washington, it's simple. Just grow the economy so fast that the resulting revenues will pay for it all.

Maintaining current productivity rates would bring a continuation of the 2 percent economic growth rates that have prevailed over the past 25 years. As explained in the next section, pushing sustained economic growth rates up to 3 percent—which is a much greater jump than it may seem—would require nearly doubling long-term productivity growth rates. Nevertheless, such bold assumptions have long been a staple of GOP budgets. Major Republican tax cuts in 1981, 2001, and 2017 were each accompanied by assurances of colossal economic booms that would bring enough tax revenue to pay for the policies.

In the new administration, Treasury Secretary Scott Bessent is targeting sustained economic growth rates of 3 percent. The most recent House Republican budget resolution assumes that rapid economic growth will save $3 trillion over the decade, as well as possibly finance $4 trillion in tax cut extensions. The budget blueprint drafted by Trump's Office of Management and Budget (OMB) Director-designee Russ Vought during the Biden administration also assumes just under 3 percent annual economic growth, shaving nearly $4 trillion off the ten-year deficits. Not to be outdone, former presidential candidate Vivek Ramaswamy absurdly promised "over 5 percent" annual growth rates. Today's GOP Congressional meetings and briefings are dominated by expectations of sustained economic growth rates of 3 percent to 4 percent. Such aggressive boasting is framed as optimistically "betting on America," while critics are dismissed as cynics ignoring the ingenuity of American workers.

In reality, these politician promises of aggressively accelerated economic growth are a lazy, longstanding gimmick meant to avoid the hard choices of restraining deficits and paying for their expensive proposals. They are based on little more than politicians' wishful thinking and over-exuberant faith in the brilliance of their own policy agendas.

No magical economic growth lever exists in Congress or the White House. Economists can analyze which economic systems produce long-term prosperity, including whether or not certain policies are generally pro-growth. However, short- and medium-term economic growth rarely behaves according to forecasting models. Keynesian models tend to wildly overstate the growth effects of government stimulus spending, while supply-side and neo-classical models have often overstated the broader macroeconomic effects of tax changes. Ultimately, the gross domestic product is determined by 330 million Americans working, spending, investing, and creating, while also interacting with a global economy. Productivity and business cycles cannot be reduced to simple policy-response models.

That does not stop politicians from guaranteeing unparalleled prosperity—even as the promised land never arrives. Average economic growth rates in the five years following the 1981, 2001, and 2017 tax cuts roughly matched those of the five years before the tax cuts. And even when federal policy changes were followed by healthy economic growth, the surge typically lasted only a few years. Since 2001, the economy has grown by an average of 2.1 percent and reached 3 percent only four times—typically due to temporary cyclical factors such as the recovery from a recession.

There is little economic basis to expect permanent, sustained 3 percent growth rates to result from extending the 2017 tax cuts, repealing taxes on tips, overtime, and Social Security benefits, providing some regulatory relief, and imposing steep tariffs. Sure, policymakers should aspire to such growth, yet basing the federal budget on that assumption is reckless.

Why Growth Rates May Disappoint

Population stagnation will likely put significant downward pressure on growth over the next several decades. Mathematically, long-term economic growth is a product of the growth rates of the labor force (measured as the total number of hours worked) and labor productivity (how much is produced per hour). If each variable grows by 2 percent, the economy will grow by a little more than 4 percent.

Past aggressive economic expansions were often heavily influenced by rapid labor force growth. The average 3.9 percent annual economic growth that prevailed from 1950 through 1980 occurred as more women and eventually baby boomers were joining the workforce (although productivity was also elevated due to a burst of new postwar technologies). However, the size of the workforce has since leveled off and may even begin declining. The Congressional Budget Office (CBO) projects that over the next decade, the U.S. population will nudge upward from 350 million to 364 million—and then remain around that figure for the rest of the century. Moreover, within a decade, deaths are set to begin outnumbering births in the U.S., meaning that immigration will be the only factor preventing a significant decline in the U.S. population. As the total population stagnates, the number of workers may decline due to baby boomer retirements—the percentage of Americans ages 65 and older is in the process of nearly doubling from 12 percent in 2007 to 22 percent by mid-century.

Reversing this workforce decline requires some combination of higher fertility rates, raising the labor force participation rate (most likely among retiring baby boomers), and expanded immigration. Instead, the Trump administration is seeking to significantly curtail even legal immigration and deport as many as 20 million undocumented immigrants. Such a policy would bring a declining workforce size.

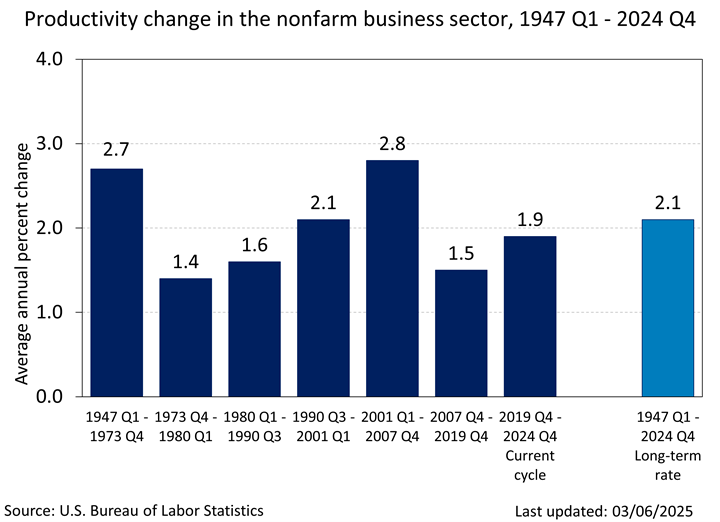

A zero-growth workforce would force all long-term economic growth to come from productivity growth. However, aside from a late 1990s/early 2000s technology-powered expansion, annual labor productivity growth has averaged 1.6 percent since 1973. Achieving consistent 3 percent economic growth—without expanding the labor force—would thus require roughly doubling the economy's productivity rate. These rates occasionally spike for a year or two, yet a permanent doubling seems unlikely in the current economy.

Artificial intelligence (AI) enthusiasts respond that the "current economy" is irrelevant because we are on the cusp of revolutionary technological changes that will unleash unprecedented prosperity. But perhaps some humility is necessary before declaring the arrival of a historic productivity utopia based on a young technology that remains mostly theoretical, vague, and years away from widespread business adoption. After all, the mainstream adoption of computing and internet technology was also expected to revolutionize American productivity. Instead, a healthy productivity bump phased down after a dozen years. AI's real-world business applications are even less developed at this point. So while an AI-based boom would be welcome, it should not be automatically assumed.

Nor is President Trump's agenda likely to maximize America's growth potential. Even with smart policies encouraging capital investment and job training, labor productivity rates are difficult to reliably improve. They are especially difficult to expand by building an economic wall around the country with steep tariffs, and expanding the budget deficit high enough to raise interest rates and crowd out investments. That leaves labor force growth, where pro-growth lawmakers would be wise to encourage high-skilled immigration, resist mass deportations, phase in a higher Social Security eligibility age (also necessary to keep the program solvent), and consider ways to address sluggish fertility rates. Without more workforce growth, even maintaining 2 percent economic growth rates may become an uphill climb—as Japan's aging economy has shown.

Even Healthy Growth Can't Finance Washington Bloat

Perhaps my economic analysis is too pessimistic. For the sake of argument, let's imagine a world where Trump's economic policies or an AI revolution nearly double productivity growth rates and thus produce sustained 3 percent economic growth despite the labor force headwinds. Would such growth provide enough budget savings to finance the Trump agenda and prevent deficits from escalating?

Unfortunately, the answer is still no. Calculations from the OMB show that permanently elevating annual economic growth rates from 2 percent to 3 percent would produce annual new tax revenues of $100 billion to $200 billion during Trump's current presidential term, swelling to roughly $700 billion a decade from now. However, while revenues would grow quickly over time, so would the offsetting budgetary costs. Long-term Social Security expenses would climb because benefits are based on wage growth that also rises with faster economic growth (which is why improved economic growth would not significantly improve Social Security finances). Medicare and broader healthcare consumption also typically grow with rising incomes. Most importantly, faster economic growth tends to increase the demand for capital, which in turn raises interest rates. A corresponding 1 percent jump in interest rates would produce enough new national debt interest costs to consume the vast majority of first-decade growth revenues.

Obviously, lawmakers should continue to prioritize productivity and economic growth because that will ultimately determine the scale of America's long-term prosperity. Economic growth can solve a lot of problems, but entitlement-and-interest-driven budget deficits leaping towards $4 trillion within the decade is not one of them. The CBO projects $22 trillion in ten-year deficits under current law, and Trump has proposed adding $9 trillion in tax cuts, with Senate Republicans also considering a defense spending expansion as large as $6 trillion over the decade. Achieving sustained 3 percent economic growth would raise approximately $3.5 trillion in new ten-year revenues and then surrender a significant portion of those savings to the aforementioned Social Security, Medicare, and interest cost expansions. In other words, even strong growth revenues would finance only a small fraction of the Trump/GOP policy agenda and none of the underlying baseline deficits that are growing so quickly.

Aim High, but Budget Cautiously

It is easy and popular for lawmakers to make budget-busting pledges and then dismiss cost concerns with misty-eyed "I believe in America" fantasies of blistering economic growth rates. Indeed, the American economy has long outperformed the rest of the world, producing one-quarter of the current global GDP. While lawmakers should continue to pursue pro-growth economic policies, they should also have the humility to acknowledge that economic performance rarely follows its predicted path. Enacting either major party's favored economic policies has rarely brought long-term booms, and economic growth progress has often been measured in tenths of a percentage point.

A family should not purchase a home it cannot afford in the hope that their salaries will somehow double next year. Similarly, lawmakers should not enact trillions of dollars of unaffordable policies in the hope that productivity growth rates will somehow quickly double—especially when there is no backup plan if such a boom never materializes.

For nearly half a century, lawmakers have "paid for" budget-busting bills with empty economic growth fantasies that ultimately saddled America with a $29 trillion national debt. There is no easy shortcut to stabilizing budget deficits—lawmakers will have to restrain popular spending programs and raise more tax revenues. These lawmakers should aggressively pursue deficit reduction policies and then treat any future economic growth revenue surge as a bonus, allowing them to scale back such fiscal consolidations.

Continuing to spend money today based on future revenues that are unlikely to materialize is just an empty—and expensive—Washington gimmick.

{kind=link}