No, 20 Million Haven't "Gained Coverage" Under Obamacare

A report in the New England Journal of Medicine tallies up the various ways that Obamacare has expanded health insurance coverage and estimates that a total of 20 million people have "gained coverage under the ACA" as of May 1. It's a count of people obtaining coverage, whether or not they had it before, not people who were previously uninsured, and it's meant to suggest the sweep of Obamacare's impact following its first enrollment period. But the sources used for this tally don't offer the kind of precision necessary to be confident in the headline estimate. It's not possible to pin down the exact number of people covered because of the law, but this figure is almost certainly overstated.

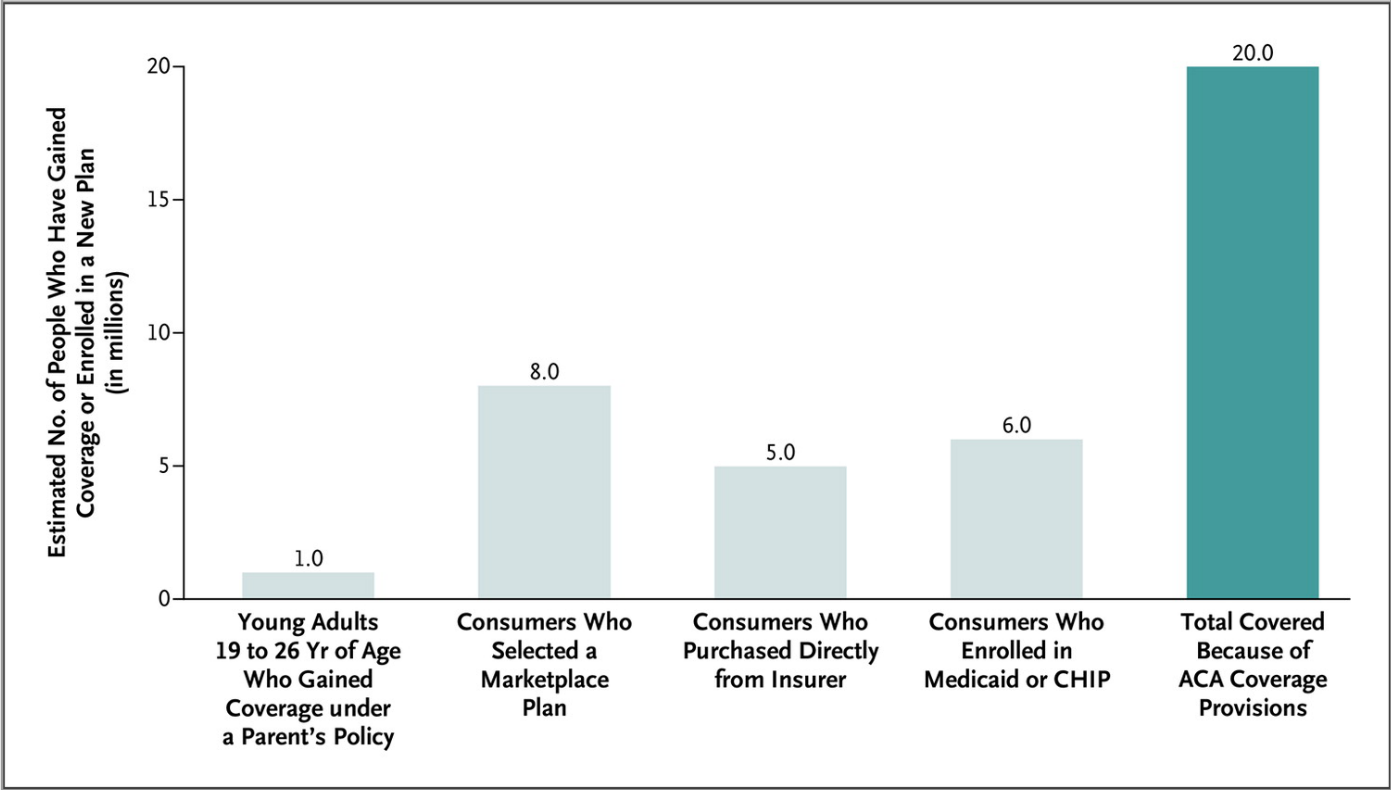

Here's the graph showing where the figures come from.

Let's start with the 1 million young adults. That number is related to Obamacare's requirement that insurers carry adult dependents up to age 26, and it's lower than the 3 million the administration has long claimed from that provision, based cherry picked year-to-year comparisons. The 1 million figure is within the realm of plausibility, but it still might be high. As Avik Roy of the Manhattan Institute has noted, the only way you get to roughly one million here is if you credit Obamacare's requirement for essentially the entire recent expansion of coverage amongst young adults. So, sure, a million is possible—but it's also possible that the number is quite a bit smaller.

The next figure, which adds 8 million marketplace sign-ups into the mix, comes from the administration's reporting on how many people have signed up for private coverage through the law's health exchanges. But as the authors note in the article, that figure doesn't account for people who signed up and didn't pay, which, based on government and insurance industry estimates, will likely cut 10 to 15 percent from the total. That would bring the total closer to 7 million (and that ignores the potential for attrition due to non-payment in later months).

The article also count 5 million covered via purchase directly from an insurer—that is, people who bought individual insurance, but not through the law's exchanges. As The Washington Post's Glenn Kessler pointed out recently when examining a similar coverage claim from the administration, these plans are not an obvious choice for inclusion:

Off-market plans are sold directly by insurance brokers or insurance companies, meaning they generally do not qualify for Obamacare subsidies. (An insurance agent could help someone enroll on an exchange if they have proper certification.) But off-market plans do include the protections included in the law, such as guaranteed coverage for people with preexisting conditions and a package of essential benefits.

Still, CBO calculated that the number of off-exchange plans would drop from about 10 million to 5 million as people moved to buying insurance on the exchanges. So why should she tout a figure that was due to go down because of the law, especially because she said she was talking about people with "affordable coverage"?

Finally, the graph cites 6 million enrollments in Medicaid or CHIP (the Children's Health Insurance Program). That number presumably comes from a June administration report stating that, nationwide, Medicaid enrollment has increased by 6 million following Obamacare's open enrollment period. But this number, too, likely overstates Obamacare's direct effect on the expansion.

For one thing, it includes people who were previously eligible for Medicaid, and merely signed up after October. For another, as the authors note in the article, it includes people in states that did not expand Medicaid under Obamacare (although the administration reports that sign-ups rose much faster, at a rate of 15.3 percent, in states that participated in the expansion, compared with 3.3 percent in non-expansion states). The administration's report also says that states are still reporting Medicaid figures in a variety of different ways, and thus cautions that this "limits the conclusions that can be drawn from the data." Even the administration does not seem to want to claim the entire 6 million: "It is important to note that multiple factors contribute to the change in enrollment between April 2014 and the July-September 2013 baseline period," the report says, "including but not limited to changes attributable to the Affordable Care Act." Obamacare was part of the story—but not all of it.

It seems clear that millions of people, some of whom were previously insured and many who were not, did in fact obtain health coverage through Obamacare's various coverage-expanding provisions. But it's too early to say exactly how many so far—only that 20 million is almost certainly an overstatement.