Obamacare's Very Bad Week at the Polls

Last week, as a sort of prologue to the rollout of the big marketing push for Obamacare, President Obama gave a brief speech touting of the law's provisions. There wasn't much new in the speech, which consisted mostly of familiar White House talking points about the health law. A small part of the emphasis, though, was on the ways the administration says the law will help ordinary, middle-class Americans. For those folks, Obama said, "the law is working the way it was supposed to."

But as we close in on the start date for Obamacare's coverage expansions, the middle class increasingly seems to disagree. A National Journal/United Technologies poll released earlier this week found that 49 percent of respondents said they believed the law would make things worse for the middle class, while just 36 percent said they thought it would help. That represents a big drop in expectations for the law in less than a year: Last September, 45 percent thought it would help.

Americans aren't just skeptical that the law will help the middle class, generally. They're skeptical that the law will help them, as individuals. In a CBS News poll out this week, 38 percent of respondents said they thought the law would hurt them personally. Just 13 percent thought it would help. About 40 percent thought the law would have no impact on them personally. That's not a huge blow for the law, exactly, but it probably works against the administration overall: How supportive will those Americans be of a law they see as making no difference in their own lives?

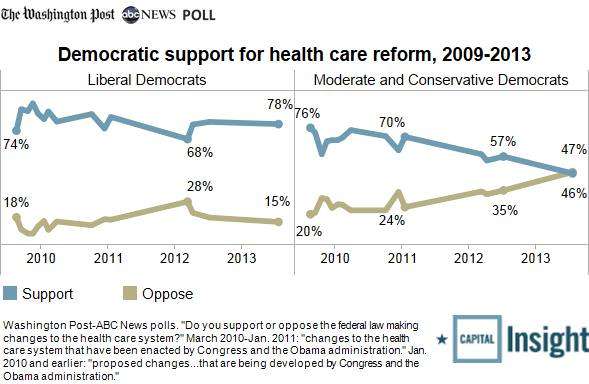

Nor is that the only bad news for Obamacare in polling this week. As both J.D. Tuccille and I noted, The Washington Post published a report yesterday finding that support for the law had dropped amongst moderate and conservative Democrats. Support amongst that group has dropped by 11 points since last year. Support amongst more liberal party members still remains strong. But overall, support amongst self-identified Democrats as a whole has dropped from 68 percent to 58 percent in the last year, according to The Post.

In the speech on Thursday, Obama lamented that "despite all the evidence" that the law is working as intended for the middle class, Republicans in the House had once again voted to dismantle the law. "We're refighting these old battles," he said. "Sometimes I just try to figure out why. Maybe they think it's good politics." If so, I suspect they are correct.