What happens when you borrow the equivalent of your annual income and those low, low teaser rates start to increase? Congratulations, America, you're about to find out.

The Wall Street Journalreports some non-shocking, non-surprising news:

Wisconsinart, Dreamstime.com

In 2017, interest costs on federal debt of $263 billion accounted for 6.6% of all government spending and 1.4% of gross domestic product, well below averages of the previous 50 years. The Congressional Budget Office estimates interest spending will rise to $915 billion by 2028, or 13% of all outlays and 3.1% of gross domestic product….

It will spend more on interest than it spends on Medicaid in 2020; more in 2023 than it spends on national defense; and more in 2025 than it spends on all nondefense discretionary programs combined, from funding for national parks to scientific research, to health care and education, to the court system and infrastructure, according to the CBO.

A quick recap of our dismal national finances: The U.S. economy generates about $21 trillion in annual activity. Debt owed to the public comes to about $15.5 trillion, but when you add intra-governmental debt (which you should, because it represents actual commitments to pay), the figure is…about $21 trillion.

This is not good, both for obvious and and for less obvious reasons. Among the obvious problems: When you have to pay more in interest, it crowds out your ability to spend on other things. If you're a government, it also might mean that you raise taxes or inflate your money. (You could also cut spending, but politicians tend to resist that for as long as possible.)

The federal government spends about $4.4 trillion a year, split among several categories, including what is considered "mandatory" and "discretionary." The mandatory stuff includes entitlements, such as Social Security, Medicare, and Medicaid. Congress doesn't need to vote on this spending for it to continue. Discretionary spending includes spending on the military, homeland security, schools, and other stuff that does need to get voted on. The percentage of spending that is mandatory has grown from around 30 percent in 1962 to about 62 percent of federal outlays today. Discretionary spending comes to about 30 percent, and interest on the debt rounds out the rest. Government spending will increase whether a divided government does anything or not. And, absent significant changes in current law, what the government spends on will be more and more limited. From a libertarian perspective, less government spending is a good thing, but we're not really going to get that, even with a gridlocked Congress.

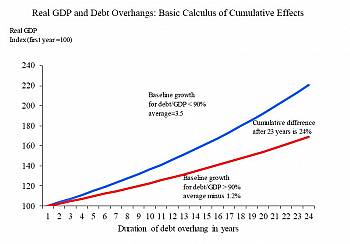

More importantly and less obviously, high levels of national debt exert a downward pressure on long-term economic growth. In a 2012 paper, economists Carmen Reinhart and Kenneth Rogoff define a "debt overhang" as a situation in which the debt-to-GDP ratio exceeds 90 percent for five or more consecutve years. After looking at 26 debt overhangs in 22 advanced economies since 1800, they conclude that "on average, debt levels above 90 percent are associated with growth that is 1.2 percent lower than in other periods (2.3 percent versus 3.5 percent)." These overhangs last a long time—in their sample, the average lasted 23 years—creating a cumulative loss in economic growth that's "nearly a quarter below that predicted by the trend in lower-debt periods."

That work has been validated by left-wing economists associated with the University of Massachusetts, who were critiquing an earlier version of Rinehart and Rogoff's work that had mistakenly found that debt overhangs reduced growth below zero. The critics conclude that "the average real GDP growth rate for countries carrying a public-debt-to-GDP ratio of over 90 percent is actually 2.2 percent.

Whether or not there is anything magical about 90 percent, there's every reason to be concerned when the government is spending far more than it can ever collect in taxes. We're essentially entering an era where "debt overhang" is the new normal and there's no sign that's going to change any time soon.

Two percent growth isn't nothing, of course. But it's well below the historical average since World War II, and the difference really compounds over the years:

Reason.com

We're already poorer for lower economic growth, even as the government spends more (and borrows more to cover those costs). The Congressional Budget Office (CBO) says the economy grew by 3.1 percent in 2018, but it estimates that annual growth is going to slow to 1.7 percent annually between 2023 and 2028.

Bonus link: More than seven years ago, Mercatus Center economist and Reason columnist Veronique de Rugy and I explored a way to balance the budget without raising taxes. Check that out here.

CORRECTION: Carmen Reinhart's name was misspelled in the original post.