The Volokh Conspiracy

Mostly law professors | Sometimes contrarian | Often libertarian | Always independent

Instant Analysis of Texas v. U.S. (Obamacare Decision) Part II: The Merits

The 5th Circuit follows NFIB v. Sebelius: the ACA can no longer be read to offer a choice between buying insurance and paying a penalty.

The Fifth Circuit decided Texas v. United States, the challenge to the constitutionality of the ACA. The panel divided 2-1. Judges Elrod and Engelhardt found that (1) the Plaintiffs have standing, (2) the individual mandate was unconstitutional, but (3) remanded for further proceedings on severability. Judge King dissented. My first post considered whether the individual plaintiffs have standing. This post will consider the merits. A third post will address severability.

The majority's merits analysis begins at p. 33. The dissent's merits analysis begins at p. 78.

As a threshold matter, the two opinions disagree about whether the ACA imposes a mandate, or merely offers people a choice: purchase insurance or pay a penalty. The Obama administration forcefully advanced the latter position in NFIB. (I addressed this issue at some length in a post titled, The Affordable Care Act Imposes A Mandate. Not a Choice.)

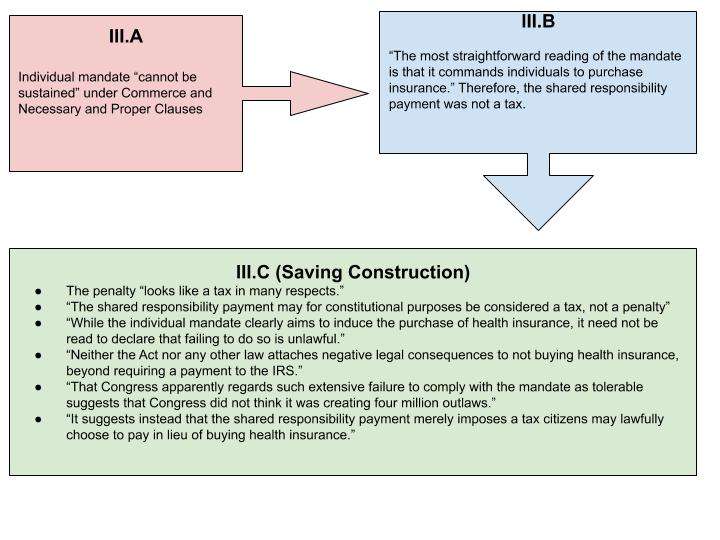

Part III-A of Chief Justice Roberts's controlling opinion ruled that this "option" reading was not the most natural way to read the ACA. Rather, the ACA is most "naturally" read as imposing a command to buy insurance. The Court only accepted the "option" argument in Part III-C for purposes of the saving construction. Judge Elrod laid out the structure of NFIB:

As a general overview, Chief Justice Roberts's opinion functioned in the following way. In Part III-A, Chief Justice Roberts said that the individual mandate was most naturally read as a command to buy insurance, which could not be sustained under either the Interstate Commerce Clause or the Necessary and Proper Clause. Though no Justice joined this part of the opinion, the four dissenting Justices—Justices Scalia, Kennedy, Thomas, and Alito—agreed with Part III-A in a separate opinion. In Part III-B, the Chief Justice wrote that even though the most natural reading of the individual mandate was unconstitutional, the Court still needed to determine whether it was "fairly possible" to read the provision in a way that saved it from being unconstitutional. In Part III-C, the Chief Justice—joined by Justices Ginsburg, Breyer, Kagan, and Sotomayor—concluded that the provision could be construed as constitutional by reading the individual mandate, in conjunction with the shared responsibility payment, as a legitimate exercise of Congress' taxing power. This last part of the opinion supported the Court's ultimate judgment: that the individual mandate was constitutional as saved.

I've created a diagram to explain Part III of Chief Justice Roberts's controlling opinion.

The mandate/option debate now turns on the status of Part III-C of the controlling opinion. Judge Elrod first focuses on Part III-B, which established the predicate for the saving construction:

In Part III-B, again joined by no other Justice, Chief Justice Roberts concluded that because the individual mandate found no constitutional footing in the Interstate Commerce or Necessary and Proper Clauses, the Supreme Court was obligated to consider the federal government's argument that, as an exercise in constitutional avoidance, the mandate could be read not as a command but as an option to purchase insurance or pay a tax. This "option" interpretation of the statute could save the statute from being unconstitutional, as it would be justified under Congress' taxing power. . . .

But this "option" reading is only feasible if the shared-responsibility payment raises revenue.

In Part III-C, the Chief Justice—writing for a majority of the Court, joined by Justices Ginsburg, Breyer, Sotomayor, and Kagan—undertook that inquiry of determining whether it was "fairly possible" to read the individual mandate as an option and thereby save its constitutionality. Chief Justice Roberts reasoned that the individual mandate could be read in conjunction with the shared responsibility payment in order to save the individual mandate from unconstitutionality. Read together with the shared responsibility payment, the entire statutory provision could be read as a legitimate exercise of Congress' taxing power for four reasons. First and most fundamentally, the shared-responsibility payment "yield[ed] the essential feature of any tax: It produce[d] at least some revenue for the Government."

In short, Part III-C established that the ACA could be read as offering an "option" to pay a tax because the shared-responsibility payment raises revenue. The choice argument only works within the context of the saving construction.

Judge Elrod reasons that the saving construction is no longer applicable, because the shared-responsibility raises no revenue.

Now that the shared responsibility payment amount is set at zero,34 the provision's saving construction is no longer available. The four central attributes that once saved the statute because it could be read as a tax no longer exist. Most fundamentally, the provision no longer yields the "essential feature of any tax" because it does not produce "at least some revenue for the Government."

Therefore, NFIB foreclosed the "option" reading of the ACA if the saving construction falls.

As the individual plaintiffs point out, the Court interpreted the individual mandate as an option only because doing so would save it from being unconstitutional. Accordingly, the intervenor-defendant states must show that the "option" would still be a constitutional exercise of Congress' taxing power.

And the majority holds that they cannot make this showing.

The dissent adopts an alternate argument advanced by the House of Representatives: the saving construction still applies, because it has become a part of the statutory scheme. Judge King wrote:

The majority pushes aside NFIB's construction, acting as though the fact that the NFIB Court applied the canon of constitutional avoidance means that its interpretation no longer governs following the repeal of the shared-responsibility payment. But when the Court construes statutes, its "interpretive decisions, in whatever way reasoned, effectively become part of the statutory scheme, subject (just like the rest) to congressional change." Kimble v. Marvel Entm't, LLC, 135 S. Ct. 2401, 2409 (2015) (emphasis added).

I'm not sure the dissent's application of Kimble to the ACA is correct. Kimble considered whether to overrule Brulotte v. Thys Co.(1964). This case provided a construction of federal patent law. Justice Kagan explained in her majority opinon:

Brulotte had read the patent laws to prevent a patentee from receiving royalties for sales made after his patent's expiration. . . . To arrive at that conclusion, the Court began with the statutory provision setting the length of a patent term. See id., at 30 (quoting the then-current version of §154). Emphasizing that a patented invention "become[s] public property once [that term] expires," the Court then quoted from Scott Paper: Any attempt to limit a licensee's post-expiration use of the invention, "whatever the legal device employed, runs counter to the policy and purpose of the patent laws." In the Brulotte Court's view, contracts to pay royalties for such use continue "the patent monopoly beyond the [patent] period," even though only as to the licensee affected. 379 U. S., at 33. And in so doing, those agreements conflict with patent law's policy of establishing a "post-expiration . . . public domain" in which every person can make free use of a formerly patented product. Ibid.

The Court suggests that Brulotte may not have been correct as an original matter, but declines to overrule this statutory decision. Here is the full paragraph that Judge King's dissent quotes from:

What is more, stare decisis carries enhanced force when a decision, like Brulotte, interprets a statute. Then, unlike in a constitutional case, critics of our ruling can take their objections across the street, and Congress can correct any mistake it sees. See, e.g., Patterson v. McLean Credit Union, 491 U. S. 164 –173 (1989). That is true, contrary to the dissent's view, see post, at 6–7 (opinion of Alito, J.), regardless whether our decision focused only on statutory text or also relied, as Brulotte did, on the policies and purposes animating the law. See, e.g., Bilski v. Kappos, 561 U. S. 593 –602 (2010). Indeed, we apply statutory stare decisis even when a decision has announced a "judicially created doctrine" designed to implement a federal statute. Halliburton, 573 U. S., at ___ (slip op., at 12). All our interpretive decisions, in whatever way reasoned, effectively become part of the statutory scheme, subject (just like the rest) to congressional change. Absent special justification, they are balls tossed into Congress's court, for acceptance or not as that branch elects.

Extending Kimble to NFIB is a stretch. First, Brulotte was a run-of-the-mill statutory decision that interpreted federal patent law. NFIB decided whether a federal law was consistent with the Constitution. Second, Kimble concerned whether stare decisis was warranted for an old statutory interpretation decision. Kimble, as applied to NFIB, does not implicate stare decisis; rather the question is whether the saving construction still ought to apply. Third, the Kimble court construes Brulotte as creating a "judicially created doctrine" to interpret a federal statute. But NFIB's saving construction was canon of avoidance to prevent a constitutional violation. Judge King puts far too much weight on the phrase "effectively" in "effectively becomes part of the statutory scheme." I don't think Kagan's opinion can bear the weight of NFIB. The saving construction exists so long as it can reasonably save the ACA. But no longer.

Judge Elrod offers this response to Kimble:

The dissenting opinion justifies its continued reliance on the saving construction—even though it is no longer applicable—by citing Kimble v. Marvel Entm't, LLC,135 S.Ct.2401(2015).This approach fares no better. The dissenting opinion quotes Kimble to say that "in whatever way reasoned," the Court's interpretation "effectively become[s] part of the statutory scheme, subject … to congressional change." Id. at 2409.The dissenting opinion correctly acknowledges that the individual mandate was never changed.But what did change was the provision that actually mattered: the shared responsibility payment. When it was set above zero, it could be saved as a tax, even though five justices agreed this was an unnatural reading. It would be puzzling if Congress could change a statute at will, entirely insulated from constitutional infirmity, just because the Court had previously used constitutional avoidance to save a previous version of the statute.

This last point is worth developing further. If the dissent is correct, and saving constructions are baked into statutes, then Congress could subsequently remove the predicate for the saving construction with impunity. Forget the ACA for a moment. Congress would now have a free pass to render a statute unconstitutional, precisely because the Supreme Court already saved it once.

Finally, the dissent argues that the individual mandate, as presently formed, is not unconstitutional because it is not an exercise of legislative power.

Thus, to my mind, the majority's focus on whether Congress's taxing power or the Necessary and Proper Clause authorizes Congress to pass a $0 tax is a red herring; the real question is whether Congress exceeds its enumerated powers when it passes a law that does nothing. And of course it does not.

The dissent relies on INS v. Chadha, and suggests that the individual mandate is a legal nullity that cannot be unconstitutional.

Congress exercises its legislative power when it "alter[s] the legal rights, duties and relations of persons." INS v. Chadha, 462U.S. 919, 952(1983);cf. id. ("Not every action taken by either House is subject to the bicameralism and presentment requirements of Art. I. Whether actions taken by either House are, in law and fact, an exercise of legislative power depends not on their form but upon 'whether they contain matter which is properly to be regarded as legislative inits character and effect.'"

What exactly is §5000A then? Neither fish nor foul? The majority responds somewhat incredulously to this position:

Finally, we would be remiss if we did not engage with the dissenting opinion's contention that §5000A is not an exercise of legislative power. This would likely come as a shock to the legislature that drafted it, the president who signed it, and the voters who celebrated or lamented it. It is not surprising that the dissenting opinion can cite no case in which a federal court deems a duly enacted statute not an exercise of legislative power, much less a statute that clearly commands that an individual "shall" do something.38

38 The dissenting opinion's theory of the "law that does nothing"results in some bizarre metaphysical conclusions.The ACA was signed into law in 2010. No one questions that when it was signed, §5000A was an exercise of legislative power. Yet today, the dissenting opinion asserts, §5000A is not an exercise of legislative power. So did Congress exercise legislative power in 2010, as seen from 2015? As seen from 2018?Does §5000A ontologically re-emerge shoulda future Congress restore the shared responsibility payment? Perhaps, like Schrödinger's cat, §5000A exists in both states simultaneously. The dissenting opinion does not say. Our approach requires no such quantum musings.

I admit I am partial to this analogy, because I described §5000A in very similar terms:

I close this section with a constitutional riddle. In 2018, the individual mandate was constitutional because the shared responsibility payment was greater than $0. In 2019, the individual mandate became unconstitutional because the shared responsibility payment dropped to $0. But what if Congress, in 2020 or later, increases the shared responsibility payment above $0. At that time—unless the Supreme Court says otherwise—the individual mandate becomes constitutional again. We would have something akin to Schrödinger's cat, where the mandate fluctuates between constitutional and unconstitutional, depending on the price of the penalty. The answer to this dilemma lies in a simple but widely misunderstood aspect of federal jurisprudence: all courts, including the Supreme Court, cannot and do not actually strike down laws. Statutes remain on the books until they are repealed. The judiciary lacks what Jonathan Mitchell referred to as the writ of erasure.163 Indeed, the Court has already considered the constitutionality of Schrödinger's mandate.

Judge King responds:

Lest the majority mistake my position and end up shadowboxing with"bizarre metaphysical conclusions,""quantum musings,"or ersatz inconsistencies, Maj. Op. at 44 & n.40 [sic, should be fn. 40], I need to make something explicit at the outset.The TCJA did not change the text or the meaning of the coverage requirement, but it did change the real-world effects it produces. Before theTCJA, the two options afforded by the coverage requirement—purchasing insurance or making a shared-responsibility payment—were both burdensome, but Congress could force individuals to choose one of those options by exercising its Taxing Power. Today, the shared-responsibility payment's meaning has not changed—it still gives individuals the choice to purchase insurance or make a shared-responsibility payment—but the amount of that payment is zero dollars, which means that the coverage requirement now does nothing. The majority's contrary conclusion rests on the premise that the coverage requirement compels individuals to purchase health insurance. With this understanding, the majority says that the coverage requirement does exactly what the Supreme Court said it cannot do: compel participation in commerce. See NFIB, 567 U.S. at 552 (opinion of Roberts, C.J.); id. at 652-53 (joint dissent). This conclusion follows fine from the premise, but the premise is wrong. Despite its seemingly mandatory language, the coverage requirement does not compel anyone to purchase health insurance.

Footnote 10 states the crux of the dissent, and indeed reflects what many see as a frustrating aspect of this case:

10. In litigation generally, and in constitutional litigation most prominently, courts int he United States characteristically pause to ask: Is this conflict really necessary?"Arizonans for OfficialEnglish v. Arizona, 520U.S. 43, 75 (1997). The majority would do well if it paused to ask whether it is necessary for a federal court to rule on whether the Constitution authorizes a $0 tax or otherwise prohibits Congress from passing a law that does nothing. The absurdity of these inquiries highlights the severity of the majority's error in finding the plaintiffs have standing to challenge this dead letter.

I hope to have more to say about the merits later. I will soon move onto a post on severability.