A Troubling Number of Young People Expect Social Security To Be a 'Major Source' of Retirement Income

Twenty-five percent of young adults anticipate paying for retirement with Social Security benefits. The number should be zero.

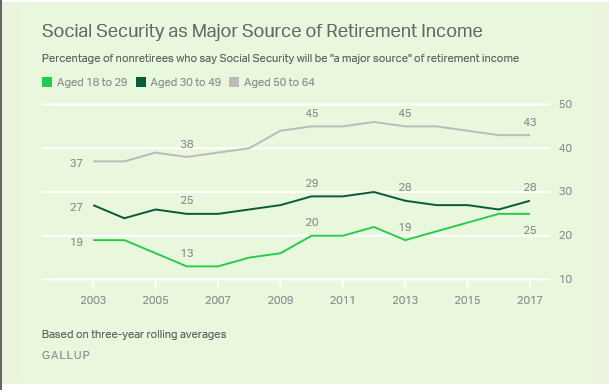

The prognosis for Social Security has not improved one bit since Vice President Al Gore promised to put it in a lockbox nearly two decades ago, yet 25 percent of Americans between the ages of 18 and 29 expect to rely on Social Security benefits in retirement. According to Gallup, which released this survey data late last month, 25 percent represents an all-time-high display of confidence for that age bracket since the group began polling on the question:

"This has occurred even as Congress and previous presidents have taken no significant steps to address the looming issue of projected shortfalls in Social Security funds," Gallup notes. So what phenomenon has convinced 25 percent of young people to believe Social Security will be there when they retire, when realistically the number should be zero?

Gallup's data tracks pretty neatly with the national conversation about Social Security's long-term viability. The decline in 25-to-35-year-olds' confidence in Social Security began in 2005, when President George W. Bush announced Social Security reform would be his top domestic priority. Faith in the program bottomed out during Bush's promotional tour for personal retirement accounts. By 2007, when young people's confidence began to climb back up, Bush's reforms were dead and buried. That confidence continued to climb through the financial crisis, and aside from a brief dip in 2013, has steadily increased since then. (Whatever financial anxiety President Trump has inspired with his erratic behavior, he has promised not to touch Social Security.)

It doesn't necessarily follow from this that young people are opposed to reforming the program. In May 2009, the Center for American Progress (CAP) released survey data collected from 915 Americans aged 18 to 29. "What is most important about these voters is not their current predilection for Democratic candidates," the survey authors wrote, "but rather the deeply held progressive beliefs underlying their voting preferences."

One of those beliefs: that "Social Security should be reformed to allow workers to invest some of their contributions in individual accounts," a "conservative position" (in CAP's words) that garnered support from 64 percent of the young people they surveyed.

Now is an excellent time to remind working age Americans that Social Security is not a sufficient primary income for today's retirees, and likely won't be for future retirees. While very few Americans of any age are prepared for retirement, millennials are better positioned than most to set up alternate streams of retirement income. As of right now, most of us aren't saving nearly enough using tax-advantaged savings accounts, but we have time. We should not spend it waiting for decisive action on Social Security, be it Bush-style reform or the opposite.