Insider Trading Is Really Common. Awesome!

A new study finds that insider trading is extremely common. CNBC Squawk Box co-anchor Andrew Ross Sorkin writes up the findings:

Now, a groundbreaking new study finally puts what we've instinctively thought into hard numbers—and the truth is worse than we imagined.

A quarter of all public company deals may involve some kind of insider trading, according to the study by two professors at the Stern School of Business at New York University and one professor from McGill University. The study, perhaps the most detailed and exhaustive of its kind, examined hundreds of transactions from 1996 through the end of 2012.

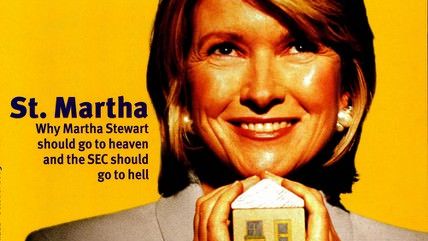

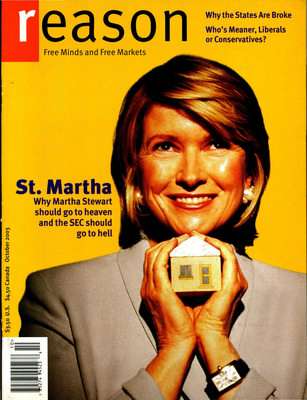

But is all this insider trading really bad news? At Reason, we have a long history of sticking up for insider trading, even making Martha Stewart our cover girl after she got into hot water with the Securities and Exchange Commission (SEC) in 2003.

That's because insider trading is a victimless crime. Markets run on asymmetrical information. Stock prices bounce around because investors are always doing their best to use their own superior information for personal gain. So-called insider information is just one kind of asymmetry, and not a particularly insidious one.

What's more, insider trading tends to make markets more efficient. Here's The Washington Post last year, taking a page from George Mason economist Henry Mannes' book:

Markets work best when goods are priced accurately, which in the context of stocks means that firms' stock prices should accurately reflect their strengths and weaknesses. If a firm is involved in a giant Enron-style scam, the price should be correspondingly lower. But, of course, until the Enron fiasco was unearthed, its stock price decidedly did not reflect that it was cooking the books. That wouldn't have happened if insider trading had been legal. The many Enron insiders who knew what was going on would have sold their shares, the price would have corrected itself and disaster might have been averted.

And what this new study from Patrick Augustin of McGill University, Menachem Brenner of New York University (NYU), and Marti G. Subrahmanyam of NYU's Stern School of Business finds is that our existing laws suck at preventing insiders from cashing in, at least on certain kinds of deals. In fact, the SEC isn't even very good at preventing its own employees from engaging in trades based on special knowledge—they actually require such trades in some cases. And while enforcing insider trading laws isn't the only thing the SEC does, it's a significant chunk of the agency's $1.3 billion budget.

I'll be on CNBC to talk about the new study today in the 1:00 p.m. hour. Tune in!