Kentucky Launches Special Session to Deal With State's Public Pension Crisis

"We have a legal and moral obligation to provide and deliver on the promises that have been made," says Gov. Matt Bevin, who called the session Monday.

A few weeks after Kentucky's pension reforms were ruled unconstitutional by the Kentucky Supreme Court, lawmakers are heading into a hastily arranged special session aimed at addressing one of the nation's worst public retirement crises before the end of the year.

Gov. Matt Bevin, a Republican, called the special session on Monday evening and two pension bills were introduced late Monday night, according to the Lexington Herald-Leader. Both were subjected to committee hearings on Tuesday and could be prepared for a vote later this week, though Republican leaders in the legislature have not yet committed to voting on either bill—and may make significant changes to what's been proposed, if they do vote on them.

Though there are two bills moving, most of the attention will be focused on House Bill 1, which is a slightly modified version of the pension overhaul package that passed earlier this year, in the midst of massive protests at the state capitol, only to be struck down by the state Supreme Court. Importantly, the court ruled the previous reform unconstitutional for procedural reasons—the legislature passed the bill without waiting three days—rather than on the merits of the changes.

Like that earlier package, House Bill 1 would move future public employees into a new retirement system using a so-called hybrid cash-balance retirement plan, which retains some elements of a traditional pension and includes individual investment options similar to a 401(k) plan. Future hires know they won't lose their money—which makes the plans significantly less risky than 401(k) plans in the private sector—but taxpayers will no longer be responsible for making up the difference when the pension investments fall short of expectations. (The Pension Integrity Project at the Reason Foundation, which publishes this blog, provided technical assistance to Gov. Matt Bevin and state legislators as they crafted various pension reform proposals over the past year.)

The second bill, House Bill 2, would limit pension increases for local governments and school districts, and it would reduce a 3 percent pension boost given to teachers after 30 years of experience down to 2.5 percent.

Both are modest steps in the right direction that might help reduce long-term costs in the state pension system, but neither will solve the short-term problem of paying for benefits owed to current workers and retirees. Pensions for those groups of employees would be untouched.

"We have a legal and moral obligation to provide and deliver on the promises that have been made," Bevin said in a statement announcing the special session. "The only chance we have of doing that, is to change the system going forward."

The end of the year represents a significant deadline for the pension bills, thanks to an odd quirk in the procedural rules governing the Kentucky legislature. The state operates on a two-year budget, which is supposed to be passed during legislative sessions in even-numbered years. To ease the passage of the budget on time, the state legislature needs only a simple majority to pass appropriations bills in those years. But in odd-numbered years, like 2019, it takes supermajorities to pass those bills. In other words, passing the exact same pension bill could require a larger number of "yay" votes on January 1, 2019, than it would on December 31, 2018.

Kentucky has eight public sector pension plans, and none of them are in good shape. The state faces more than $62 billion in unfunded pension liabilities over the next few decades, and the teachers' pension plan (the Kentucky Teachers Retirement System, or TRS) accounts for more than $33 billion of that debt.

By comparison, Kentucky taxpayers paid about $32 billion last year to fund the entire state government—everything from schools to road construction.

Depending on how you measure, Kentucky's public sector pension plans are either the worst-funded or the third worst-funded in the country. A Standard & Poor's report in 2016 ranked Kentucky dead last, with just 37.2 percent of the assets needed to cover current obligations, behind even such infamous pension basket cases as New Jersey (37.8 percent) and Illinois (40.2 percent). A Moody's report published a month later measured states' pension liabilities as a percentage of their annual tax revenue. Kentucky's liabilities totaled 261 percent of annual tax revenue, well above the average burden of 108 percent and more than three times the median of 85 percent. Only Illinois and Connecticut were in worse shape.

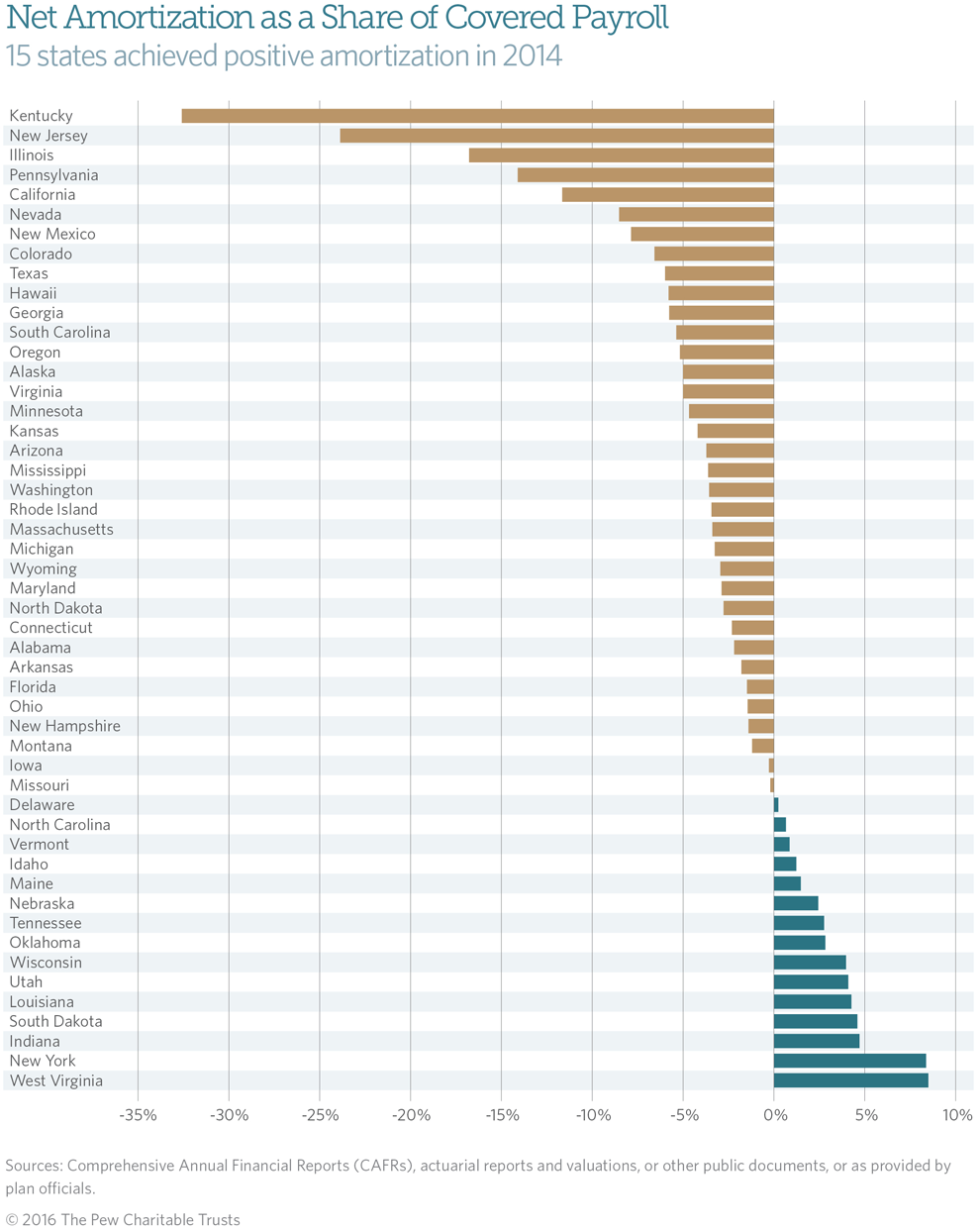

According to an analysis from the Pew Charitable Trusts, only 15 states contributed sufficient funds to their pension systems in 2014 (the most recent year for which complete data is available) to avoid falling farther behind. Among the 35 states that failed to do so, Kentucky was by far the biggest deadbeat, chipping in less than 70 percent of what is required. In the decade between 2006 and 2016, the Kentucky teachers' pension plan had negative cash flows in nine of those years, and hemorrhaged $634 million in 2016 alone.

This is a completely unsustainable course, as this chart from the state pension system makes pretty clear. If the state's teacher pension system earns only 3.8 percent annually instead of the 6 percent returns that are baked into the plan's assumptions, it will be out of money by the mid-2030s.

In other words, a new college grad hired as a teacher in a Kentucky public school is being told to trust a retirement program that will likely implode before he or she turns 40. Seems like a big leap of faith.

{kind=link}