Oil and Gas Better Than Gold

All that earns does not glitter-like oil and gas. The investor can try oil stocks, an oil income program, or public drilling programs.

Gold commands a greater value in the marketplace today, so there is obviously more incentive to produce it. Even with production costs of $300 an ounce, it has become economical to reopen old, boarded-up mines in gold-rich Nevada and Arizona. So it is with crude oil and natural gas—but even more so. Gold will fluctuate violently in price and may even slip back to $300 or $400 an ounce. Oil and gas reserves in the ground, on the other hand, are more likely to continue to command increasingly higher prices in the world marketplace.

Oil and gas possess excellent investment merit today primarily because they are such vital and universally essential commodities. Civilization, for the foreseeable future, literally cannot go on without them. Surely jetliners are unlikely to fly on nuclear energy cells for some time to come, and cars are not going to run on sunshine!

Global oil consumption is presently 23 billion barrels annually. The crude oil reserves for most OPEC countries continue to decline rapidly. For nearly a decade, America's proven reserves of oil and gas have also continued to decline. If the non-Communist-world demand does no more than maintain the status quo over the next decade, 200 billion barrels of new oil would have to be developed to maintain proven reserves at the present level.

The classic supply-demand imbalances that have created spectacular price explosions in the past clearly exist in oil and gas today. Is $100 a barrel really unthinkable? Was $800 gold? Just a couple of years ago it was indeed. Can't we assume, with a high degree of confidence, that there is the likelihood of continually rising prices for crude oil and natural gas perhaps throughout this decade?

BULLISH ON OIL

Imagine, if you will, what existing reserves in the ground would be worth today if there were widespread fears that no new significant provinces of oil and gas were to be found! Those who owned reserves would enjoy a windfall of inestimable scope. The truth is that, despite an intensification of exploration worldwide, major oil discoveries of late have been relatively few. Important finds have been made in the Canadian Arctic, Libya, Mexico, Nigeria, and Red China. Lesser oil strikes have been made off shore Brazil, India, Malaysia, and Norway.

Despite highly intensive exploratory effort during the 1970s, outside of Mexico no major oil and gas province was discovered. Numerous optimistic forecasts of substantial new reserves of oil and gas were unrealized. The immense oil and gas provinces in Alaska and the North Sea were discovered in the 1960s. Only recently have important gas discoveries in the United States been made in the Overthrust Belt of the Rockies, the Tuscaloosa Trend in central Louisiana, and in the Gulf of Mexico.

The point of this background is to impress upon you that the easily discoverable and recoverable oil has already been found. Look at where the major exploration and development activities have been going on of late: the Arctic Sea! Alaska! the North Sea! offshore Newfoundland! Each location is most inhospitable and extremely expensive to develop. In fact, the investment required to bring on production a daily single barrel of oil runs about $10,000.

Soaring prices for crude oil, in conjunction with declining reserves, have spurred unprecedented expenditures for new exploration and development. Capital requirements for the entire non-Communist oil industry have been forecasted to rise from over $20 billion this year to at least $70 billion by the end of the century. The anticipated acceleration in outlays will substantially exceed that for all industry in general.

The rapidly rising prices for crude have rendered the prospects for natural gas significantly more favorable, too. Previously uneconomical pipeline projects, requiring multibillion dollar investments, are now feasible. With 5.3 thousand cubic feet of natural gas equivalent to the energy output of a single barrel of oil, and the sharp escalation in fuel prices, there has been accelerated drilling for natural gas.

What this all means is that oil and gas reserves are an outstanding investment opportunity in this decade of energy crises. Geographic and climatic factors point to continuing price escalation and restricted availability for oil in this decade. Oil and gas reserves in the ground are likely to become increasingly more valuable. Those who recognize this opportunity, and are cognizant of the best ways to capitalize on it, will profit handsomely.

There are essentially three ways in which you can buy and own oil and gas reserves in the ground. The first way is to buy common stock in those corporations that already own extensive reserves. Another way is to buy actual producing wells, and the reserves that go with them, through an investment in an oil income program. The third way is to buy ownership interests in public drilling programs that actually drill for new reserves. Each of them provides a way to capitalize on the boom in oil and gas, but it is up to the individual to determine which is personally suitable.

TAKING STOCK

In considering being a stockholder of reserves, there are two basic concerns. First, how do you choose which company or companies to invest in among the universe of corporations owning oil and gas reserves? Second, what are the pros and cons of this method of investing vis-a-vis the other two? As an investor in common stock, you have to be up on the capital gains tax treatment and how it affects your investment planning. If your major objective is to optimize your net after-tax return on your investment, then your strategy should be to go for a one-year holding period in order to realize long-term capital gains and have 60 percent of the gain excluded.

Choosing which oil and gas companies to invest in can be simplified by subscribing to an advisory service that follows the industry. You can also monitor the research reports and recommendations from top analysts who specialize in oil and gas and publish periodic reports distributed by brokerage firms.

On the other hand, if you would like to know which companies have the greatest reserves, a service out of Greenwich, Connecticut, publishes "Oil Industry Comparative Appraisals" in John S. Herold's Petroleum Outlook. It is an annual asset appraisal of petroleum companies—large and small, domestic and foreign—based upon their reserves, acreage, production, marketing, etc., plus other net assets.

One of the features of Petroleum Outlook is data on advances in asset values of the many oil and gas companies. According to Herold's research and analysis, only nine companies have been able to increase their asset bases at an annual rate in excess of 30 percent:

Houston Oil & Minerals (85%)

Mitchell Energy (37%)

Petro-Lewis (36%)

American Quasar (34%)

Texas Oil & Gas (33%)

Southland Royalty (32%)

Wiser Oil (32%)

Great Basins Petroleum (31%)

Pogo Producing (31%)

Among the major, fully integrated oil companies, the best annual rates of advancing asset values, according to Herold, have been achieved by:

Standard Oil Ohio (22%)

Marathon Oil (20%)

Sun Company (18%)

Union Oil California (18%)

Atlantic Richfield (15%)

Shell Oil (15%)

Canadian companies that have boosted their asset values at the greatest annual rate have been Voyager Petroleum (39%), Bow Valley Industries (30%), and Pan Canadian Petroleum (28%). Among the major Canadian corporations, the best annual gains have been scored by Gulf Canada (18%), Shell Canada (17%) and Texaco Canada (15%).

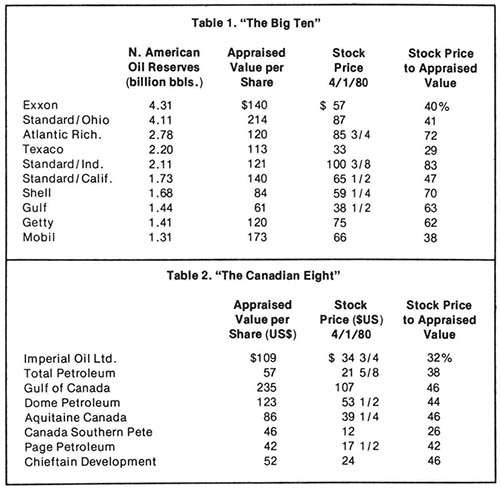

By reviewing Herold's comparative data you can fairly easily identify which companies have the greatest reserves in North America, such as in Table 1. This list is the "class" of the industry, of course. But even in choosing among these giants, you may want to know which have been experiencing significant declines in oil and gas production, despite prominent price increases, as they will have difficulty in maintaining earnings growth. Standard Oil of Indiana, Mobil, and Texaco have experienced eroding domestic oil production.

You may also prefer companies that are diversified into other energy-related fields, such as uranium and coal reserves. The standouts in that respect are Atlantic Richfield, Gulf, Exxon, and Standard Oil of California. Each ranks among the top 20 companies that control both uranium and coal reserves. In addition, these same four concerns have been working on refining processes that will be very important elements in the future of nuclear energy.

Among the foregoing "Big Ten," Atlantic Richfield (ARCO) is in an especially good position. On the Alaskan North Slope and in the Gulf of Mexico, ARCO continues to develop new oil and gas reserves. This should assure it a position among a very few companies able to increase domestic production. In addition to its immense reserves of crude oil, natural gas, coal, and uranium, its acquisition of Anaconda last year gave it a big stake in gold, silver, and copper mining, as well.

Canadian oil companies tend to be a very attractive alternative to American oil companies because of the former's vast heavy oil reserves and relatively favorable taxation rate. Canadian companies already sell their production at world prices, in contrast to US companies, which are faced with another year or so of gradual decontrol before "old" domestic oil commands world prices. Also, Washington has just imposed a discriminatory excise tax on American oil companies for their so-called windfall profits.

A.G. Becker, Inc., which closely follows the Canadian oils, also provides us with appraised valuations of reserves. Becker's valuations of the Canadians tend to be substantially higher than Herold's "Oil Industry Comparative Appraisals" because the latter gives no value to heavy oil reserves until they actually enter production. Becker assumes that a very conservative 20 percent of the in-place reserves will be recoverable, thus compensating for overestimates of the reserves. Becker's appraisals of the "Canadian Eight" are provided in Table 2.

At 44 percent of appraised value, Dome Petroleum appears to be the current standout. Dome Pete has the largest acreage holdings in Canada (estimated to be 42 million acres) and is currently the sixth-largest producer there. Dome's overall working interests in current drilling activities make use of one-tenth of all the drilling rigs in Canada. In addition, it has a one-third interest in the primary acreage of the Beaufort Sea, which is considered to have great promise for major new oil fields. Moreover, Dome recently made several sizable acquisitions totaling $2 billion, including half-interest in the largest gas pipeline company in Canada.

Overall, a shareholder in reserves, in contrast to an investor in a public drilling program or an oil income program, has the single great advantage of flexibility. The ability to trade the common stocks of the oil and gas companies obviously is attractive to many investors who would not be comfortable with their capital committed long-term under someone else's control. On the other hand, the single great drawback to the common stockholder is the lack of tax advantages. Stockholders invest or trade with after-tax dollars and enjoy neither deductions nor sheltered income.

PRODUCTION OWNER

Unlike owning shares in corporations that have reserves in the ground or investing in public drilling programs, there is a way for you to buy directly into actual reserves in the ground and enjoy tax-sheltered cash flow from your producing wells. There is no drilling for new oil involved, and there is no involvement in the stock market.

An oil income program gives you an opportunity to buy into actual reserves and existing production with an estimated commercially productive life of 12-15 years. The basis for profitability of investments in producing properties is predicated on the ability of the producing company, namely, the general partner, to buy oil and gas reserves at a price that substantially discounts the future net revenue to be realized from the sale of production. The spread between the discounted purchase price and the ultimate dollar return represents profit to you, the investor.

There is nothing unique about buying and selling of oil and gas properties by discounting the future net revenues. It is the basis on which properties have been exchanged within the oil industry for decades. Companies that specialize in exploratory or developmental drilling are happy to sell their commercially productive properties, even at a large discount, in order to plow those proceeds into new exploration and development where the greatest profit opportunities lie.

The real risk of this oil production business becomes, not whether you'll get your money back, but whether the profitability of the producing properties will be as large as anticipated. By subjecting each proposed acquisition to a number of independent evaluations by geologists and petroleum engineers, a lesser degree of significant error may be achieved. Moreover, by diversifying each limited partnership into three or more separate acquisitions, the element of risk of overestimating the reserves they are buying for you is greatly diminished.

The difference between what they pay for oil and gas reserves discounted today and what they sell it for over the next 10 or 15 years is, of course, the margin of profit to the investors. Oil-producing companies sell their oil primarily to refineries and their gas to gas distribution companies on a contractual basis. This investment is currently generating a tax-favored cash flow of 12 percent after operating costs.

Direct investments of this nature in commercially productive wells are made through the medium of the limited partnership. There are several advantages of investing in limited partnerships that you do not enjoy with common stock. First of all, you share proportionately in the revenue and the costs, thus enjoying the tax breaks on depreciation, depletion, and interest expenses. Second is the advantage of direct ownership interests in specific properties. The avoidance of stock market risk is a third advantage of limited partnerships. A final advantage is that of limited liability. The major drawback of limited partnership interests is that they tend to be illiquid and non-negotiable.

Because of the start-up costs associated with getting each partnership going, there are tax deductions generated at the outset that are either passed on to the investors immediately or amortized over an intermediate time period. These deductions serve to reduce the taxes on the cash flow of a partnership in its early years. As the partnership continues its operations, it is entitled to realize cost depletion against the production of oil and gas that is sold, as well as depreciation on the well equipment. In addition, there are deductions for the interest expenses realized from utilizing leverage through bank loans.

The effect of these factors is that most of the cash flow from the investment distributed to the limited partners is nontaxable. The amount of cash flow that is sheltered will, of course, vary somewhat from partnership to partnership. In sum, an oil income program offers several key benefits to investors interested in direct ownership of reserves: low risk, significant appreciation potential, substantially tax-sheltered cash flow. Additional advantages are a modest first-year deduction, ease of reinvestment, and ease of liquidation once the partnership is fully invested.

GOING FOR NEW RESERVES

You can invest directly in ventures that drill for new oil and gas reserves onshore in the continental United States as a limited partner in a public drilling program. Investments of this type have been called tax shelters because they have built-in tax incentives designed to entice investment capital into this relatively high-risk area. Because of the high degree of risk associated with drilling for new reserves, these public drilling programs historically have been, and still are, restricted to investors in higher tax brackets.

The principal tax incentive for oil and gas drilling programs centers around initial deductibility, depletion allowance, and capital gains. Depending on the structure of individual programs, from 50 to 100 percent of your initial investment may be deductible in the calendar year of investment. In addition, the depletion allowance provides that about one-third of your future income from a drilling program will come to you tax free. The future redemption of a drilling program limited-partnership interest in most cases will be subject to preferential capital gains tax treatment. The combined effect of these three tax incentives is to significantly enhance the already attractive economics of oil and gas drilling.

There are risks in all oil drilling. The riskiest is, of course, the so-called wild-catting in pursuit of a significant new discovery in the remote frontiers of the planet. On the other end of the risk continuum is the safest form of drilling, known as box score development, or secondary oil recovery. That means drilling in areas of widespread oil and gas deposits, resulting in a very high percentage of wells being completed but also known to result in marginal economic return.

Between these two extremes fall most of the oil and gas drilling program activities conducted by public drilling companies. There are three basic types of drilling: exploratory, developmental, and balanced, or combination, drilling.

Exploratory drilling is conducted in new areas that are believed to have a very high probability of containing hydrocarbons. Nevertheless, the industry average of commercially productive wells to dry holes is one in nine. Developmental drilling is conducted in areas proximate to existing production. The industry average is that, for every four wells drilled in an existing field, three will become commercially productive. The trade-off for the public drilling companies is the lower cost for acreage and royalties on new exploratory properties and greater potential payout versus much higher costs to drill developmental wells.

The risk-reward ratio is probably an unwritten law of economics. Risks are commensurate with the rewards. High risk, high reward; and vice versa. So it is in oil drilling. The really exploratory drilling programs will give you the maximum tax deductions and, if successful, the greatest potential payoff. If unsuccessful, however, they also have the greatest probability of loss of your entire investment. A pure developmental drilling program, on the other hand, is a relatively low-risk venture with a very high probability of realizing a good return on your investment. But then, the profit margin will be relatively low, too. The reason for this stems from the greater costs involved. As a result, few public drilling programs are purely exploratory or purely developmental.

DIVERSIFYING RISK

The balanced drilling programs are either designed to provide a 50-50 split between exploratory and developmental drilling or tend to be biased 65-35 toward either exploration or development. The intent of the balanced program is to maximize the tax write-offs and give the investor an opportunity to participate in a new discovery and, at the same time, protect the investor's capital through developmental drilling activities. The expectation is that, even if the program completely strikes out in its exploratory activities, the developmental wells will generate enough to recoup one's investment. Major brokerage firms select a few public drilling programs each year from among the 60 companies that raise money publicly. As a rule, if a drilling program is offered through a major brokerage company, it has been pretty thoroughly checked out.

When selecting a public drilling company, it is advisable to choose one that is large, consistent, and preferably a major factor in the industry. It is also a good idea to invest in one that drills only for the partnerships it manages. This will avoid conflicts of interest. You would also be better off avoiding companies that charge back acreage costs to the limited partners if the acreage proves to be worthless; it is wiser to choose a company that treats the acreage as part of its capital contribution to the program.

As a rule of thumb, the rate of return on an oil drilling program investment can be considered a success if you receive back your original investment in three to five years and a steady tax-favored cash flow thereafter. Your odds of being successful will be improved by sticking with seasoned public drilling companies that have demonstrated the capacity to successfully manage a number of drilling programs for five years or more.

To minimize the risks of these investments, it is advisable to participate in each program over a three- to five-year period. There are several advantages to doing this. First of all, you have a far greater opportunity of participating in an exceptionally successful program. Some of the programs will be mediocre, some of them will be good; but all you need is one spectacularly successful one during those three to five years to make the entire endeavor well worthwhile. Second, by participating in a series of programs, the cumulative tax advantages accrue to your advantage. Let's assume that each program will enjoy a 100 percent write-off. As an example, if you have a first-year deduction of 75 percent on your investment and a 25 percent residual write-off the second year, that 25 percent carryover will dovetail with your next year's 75 percent write-off from the second program for a total 100 percent deduction. Third, you have greater diversification of risk by participating in a series of programs over several years, eliminating the one-shot nature of an investment in a single drilling program.

A public drilling program may be suitable for you in terms of your investment objectives and financial qualifications. You must, however, consider whether you are prepared to assume the risks, the illiquidity, and the long-term commitment required for such an investment. Perhaps the oil income program would be better for you given its lower risk, greater certainty of current income, and liquidity. Then again, you may wish to simply buy stock in oil-rich corporations. Whichever way is appropriate for you is, of course, the way to go. If you can diversify your capital into all three areas, you are only expanding your opportunities to participate in the potential rewards of investing in undervalued oil reserves. You too may become convinced that black gold glitters brighter than the precious yellow.

Ray Pastor works for a securities firm in Hallandale, Florida, where he specializes in financial planning and tax-advantaged investments. He is currently working on his first book, on profiting from inflation.

This article originally appeared in print under the headline "Oil and Gas Better Than Gold."