Remdesivir Pricing

Let's assume that further studies establish that remdesivir turns out to have precisely the effects on COVID-19 patients indicated by the preliminary study reported several days ago. That is, assume that remedesivir is given only to patients whose illness is as severe as that of the patients in the initial study, and that with treatment, 8% of patients die instead of the 11.6% of patients who would have died without treatment. Also, assume that treated patients recover 31% faster than they otherwise would have. What then should a treatment of remdesivir cost?

An advocate of free markets, of course, would suggest that drugs ought to cost what people will pay for them. A truly free-market price for remdesivir would likely be quite high at least for now, because supplies are low and because there would likely be strong demand from people with much less severe cases, who might hope that remdesivir (like Tamiflu) works even better when taken early. But let's place this aside. For the most part, drug prices in the United States are not determined by how much individual consumers are willing to pay for the drugs. The drug market looks nothing like the market for houses, cars, or even over-the-counter medications.

Drug prices in the United States are determined in a market of sorts, in which Pharmacy Benefit Managers act as intermediaries between manufacturers and health insurers, but it's a very strange market. Health insurers, for example, feel that they have to make available some reasonable treatment for every condition, in part because insured patients can file for independent reviews of coverage denials on the ground that a drug was medically necessary. When our legal system effectively tells insurers that they have to offer certain drugs, it shouldn't be surprising that they will pay very high prices for those drugs. If a drug were priced well above what a cost-benefit analysis suggests is appropriate, state regulators would be less likely to sanction health insurers for refusing to offer the drug. So, there is some limit on what PBMs and ultimately insurers and uninsured consumers will pay, and the negotiations thus depend very loosely on cost-benefit concerns. Insurers agree to buy drugs not primarily because they think that offering a more attractive formulary will increase their insurance sales (though that is a consideration at the margin) but because they think they can't get away with not offering certain drugs. Russell Korobkin has done excellent work explaining limits on health insurer competition on how we might imagine health insurance markets in which health insurers actually competed on the quality of what they offered.

In the absence of a functional market, however, prices can be too low as well as too high. Pharmaceutical companies fear public outrage should they price drugs high. Outrage may make it easier, after all, for PBMs and insurers to refuse to buy the drug. And it can lead to unpleasantness like congressional investigations. Outrage is more likely to occur when pricing is more salient, and pricing will be more salient when a disease is more salient. Emergencies, meanwhile, generate outrage about price-gouging in many areas of the economy. One might think such concerns irrelevant in the pharmaceutical arena--a developer with the foresight to develop a drug that might be useful in a future pandemic and that otherwise will likely be valueless can hardly be thought to have obtained an unfair windfall--but because lives are at stake, concerns about price-gouging are especially strong.

And so we can predict that remdesivir will sell for what Gilead thinks it can get away with, whether this is more or less than the benefits that the drug produces for the patient. Part of what it can get away with, however, will depend on independent cost-benefit analyses, and an organization that produces influential, high-quality evaluations is the Institute for Clinical and Economic Review (ICER). ICER has produced a new report on pricing of remdesivir and other potential COVID-19 patients. It appropriately notes that clinical information may change but takes the same assumptions adopted above, allowing for the mortality benefits even though they do not yet meet the standard of statistical significance. It accordingly develops a model that determines an appropropriate price for remdesivir treatment: $4,460. Business Insider characterizes this price as surprisingly high and quotes a biotech analysis who sees a $1,000 price tag as "pretty reasonable." ICER also offers an additional model based on the principle of cost-recovery and produces a price of just $10 per treatment.

To me, even the higher amount seemed surprisingly low. COVID-19 is the world's most pressing medical problem. A great deal of discussion has focused on case fatality rates. Suppose that 1,000,000 seriously injured patients end up receiving remdesivir, saving 36,000 lives. In a world in which governments are spending trillions of dollars to mitigate COVID-19, can that really be worth only $4.6 billion?

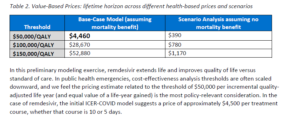

What explains the low price? The key portion of the ICER analysis is here:

The three rows of the table correspond to different possible valuations of a quality-adjusted life year (QALY). The QALY values rise linearly, considering $50,000, $100,000, and $150,000 valuations. But the middle column, which assumes the mortality benefit and reports the net treatment value, does not. With $50,000/QALY, the benefit is only $4,460, but each additional $50,000/QALY produces another $24,210 in benefits. The report does not fully explain this, but I believe this is because the model is estimating social benefits, and there would be a cost of $19,750 to administering remdesivir. Presumably, if ICAR had considered a QALY valuation of $40,000, it would have recommended that remdesivir not be administered at all, even if it could be obtained free from the manufacturer.

It thus matters a great deal in the model how one values a QALY. Timothy Taylor offers an accessible introduction to this question, noting in passing that ICER has generally used a value between $100,000 and $150,000. The paragraph below the table furnishes the critical detail: "In public health emergencies, cost-effectiveness analysis thresholds are often scaled downward, and we feel the pricing estimate related to the threshold of $50,000 per incremental quality-adjusted life year (and equal value of a life-year gained) is the most policy-relevant consideration." In other words, when large numbers of lives are at stake, we should pay less for health care, and so "we feel" that a price less than one-tenth the value we would get using the customary $100,000/QALY is appropriate.

The existence of a public health emergency should not mean that we should pay less for cures. If anything, one might think that one would pay more. After all, if we can reduce the case-fatality rate, then we might be able to open society up a little more than we otherwise would be able to. That benefit alone seems likely to be worth more than $4.6 billion. Perhaps there is a bit of a paradox: if we start to eliminate many (but far from all) COVID-19 infections, we might relax so much that we end up with even more deaths. Still, when assessing the benefits of a drug, we should probably place aside the question of whether policymakers will properly optimize the lockdown, and in any event, this played no role in the ICER analysis.

Perhaps the idea underlying ICER's view is that our pricing of medicines in a public health emergency ought not produce windfalls for producers. But strictly speaking, that should be irrelevant to a value-based assessment. Consideration of windfalls is relevant to the alternative assessment model, the one that produces a recommended price of $10. The core idea of that model is that the manufacturer should be allowed to recover R&D costs, as well as marginal costs and a small profit margin. But in this case, ICER concluded as follows:

In our base-case cost recovery calculation, we set the costs of research and development to zero. There are important reasons to assume that sunk research and development costs should not be used to help justify the price of new drugs. For remdesivir, this perspective is strengthened by the fact that it was previously developed as part of a suite of agents for potential use in chronic Hepatitis C. Given that the manufacturer successfully launched other drugs for Hepatitis C, it seems reasonable that any sunk costs for research and development have already been recouped in the successful market experience of the manufacturer's other treatments in that area. For that reason and others, we are not currently including any research and development costs separate from the development costs already captured in the cost of production. As the manufacturer spends new money going forward on clinical trials for the COVID-19 population, consideration will be given to including these costs as a possible component of a cost recovery price estimate.

The basic theory is that a company should be able to recover its R&D costs, but once it has successfully done so, it should not be able to recover any more, even if its research turns out to be useful for other diseases, indeed even if its research turns out to save the world from a pandemic. At best, it could obtain some additional recovery of its costs. The problem with logic of this sort is that it does not account for risk, and moreover risk is very difficult to account for. Those who advocate investment-based cost caps at least generally concede that these price caps must incorporate the risk of failure, so that one should receive double recovery if there was a fifty percent chance of failure. But it's very difficult retrospectively to assess, without hindsight bias, the risk of success. This is complicated further by the reality that there is a distribution of possible success levels and that this distribution is constantly changing. It's also not always obvious whether particular expenses are targeted at one disease or another. If pharmaceutical companies think that government officials will tend to underestimate risk and they expect to be able to recover only risk-adjusted costs, then they will not invest at all.

These considerations help explain the appeal of an approach that focuses on value rather than investment, even if government regulation prevents a true free market. If pharmaceutical companies expect that successful investments will be rewarded with an amount commensurate with the benefits produced by treatments, then the companies' internal cost-benefit analyses will already place an appropriate weight on considerations of risk. Meanwhile, companies will have incentives to take into account both obvious potential applications of drugs and the possibility of serendipitous applications. If we want pharmaceutical companies to develop drugs that might turn out to be extremely useful in the event of a pandemic, then a value metric helps accomplish this. We should not then subvert the value metric by smuggling in cost considerations, changing the rules for public health emergencies.

That does not imply that the market always works perfectly. Sometimes, a drug company might benefit from a truly unpredictable exogenous shock. But this is especially relevant as to investments made after the pandemic, once unexpected demand suddenly materialized. Patent law can over-reward inventions that are not obvious but that are relatively cheap. Usually, this is not a problem because patent law induces earlier invention, but we can't be sure of this when demand suddenly arises. The possibility that a pandemic might occur within the lifetime of a patent is entirely predictable, and so it's hard to see why drug companies would not take that possibility into account. Any pharmaceutical company would have assigned a relatively low probability to the expectation of a pandemic as great as COVID-19, but that militates toward greater recovery, not less.

If one contends that companies will not change their R&D behavior because pandemics are improbable and capital markets are short-sighted, one might develop an argument that investments should be a factor in drug price recovery. A very interesting recent article in the North Carolina Law Review by Miriam Marcowitz-Bitton et al., for example, argues that investment should help determine patent duration. But at the least, government should try to err enough on the high side when estimating risk that it does not end up undervaluing R&D contributions. The ICER estimates seem to me to be the opposite--quite stingy, erring intentionally on the low side out of fear that someone else might err on the high side. Those who wish to ensure robust incentives for R&D against pandemics and other critical social problems should argue for and defend considerably higher prices than the ones that ICER would think tolerable. If the government wants everyone to have access to the drugs, then it should negotiate a buy out at arms' length.