The Immense and Growing Price of "Tax Expenditures"

Tax expenditures are officially created loopholes that allow individual and corporate taxpayers to reduce their federal liabilities if they engage in certain sanctioned ways. They're called expenditures because they resemble government spending and have been treated as such in federal budgets going back to the 1970s. The biggest tax expenditures (in terms of dollars) include not counting employer-paid health premiums and insurance as compensation, excluding pension contributions and earnings from taxes, the mortgage-interest deduction on up to two homes, depreciation of machinery and equipment, deductions for state and local taxes paid by individuals, and charitable contributions.

Tax expenditures tend to be very popular with the people who benefit from them but they also represent a blatant attempt by the government to engineer behaviors ranging from having children to buying homes rather than renting. As the consensus that our current tax code is overly complicated and inefficient (both in terms of economic activity and revenue generation), all tax expenditures should be on the table for reconsideration and elimination.

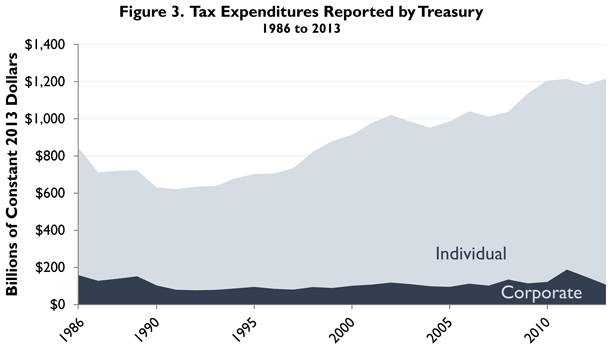

The Tax Foundation has an interesting new study out that looks at the massive increase in the value and type of tax expenditures since the last comprehensive tax reform, which took place in 1986.

Beginning in the mid- to late 1990s, numerous tax expenditures were added, expanded, or otherwise allowed to grow. Today, the tax expenditure budget is $1.2 trillion, which represents real dollar growth of 44 percent since 1986 and 96 percent growth since 1991 when tax expenditures were at their lowest. All of the growth has been in the individual tax code, with about two-thirds of real dollar growth coming from just three provisions: the earned income tax credit, the child credit, and the exclusion for employer-provided healthcare. Corporate tax expenditures have actually declined since 1986 in.

The study concludes

While [tax expenditures] may achieve some other social purpose, such as more redistribution, more healthcare, or more education, they come with many downsides relating to their implementation in the tax code, namely ineffectiveness, fraud, abuse, and overspending. One avenue for tax reform would be to move these provisions to the spending side of the ledger, overseen by a spending agency subject to the annual appropriations process rather than the IRS.

I'd argue that the best sort of tax reform would, first of all, focus on the absolute amount of revenue needed to pay for the amount of government we want to fund over a certain period of time. Because massive amounts of borrowing fund government operations (and effectively transfer taxes to future taxpayers), most politicians don't see tax policy as a way or raising a specific amount of money to pay for current government. Instead, they treat tax policy as something that should always be tweaked to squeeze more revenue out of taxpayers.

Beyond that, taxes should be simple and transparent and they should distort economic activity as little as possible. As the Tax Foundation suggests, it would be far more efficient and effective to directly subsidize transfers via clear-cut government spending rather than through confusing, ineffective, and distortionary tax policies.

Related: "Taxes: The Price We Pay for Civilization" (originally released on April 14, 2010)